Table of Contents >> Show >> Hide

- Why We Misunderstand Risk (Even When We’re Sure We Don’t)

- Two Lenses for Risk: Numbers and Narratives

- Prospect Theory: Why Losses Feel Like They Use ALL CAPS

- Reframe #1: Risk as a Design Problem (Not a Bravery Test)

- Reframe #2: Risk as a Portfolio (Diversify Your Life, Not Just Your Money)

- Reframe #3: Risk as a Conversation (Because People Don’t Follow Spreadsheets)

- A 10-Minute Risk Reframe You Can Use Today

- Common Risk Traps (and the Antidotes)

- Conclusion: The Point Isn’t Less RiskIt’s Better Risk

- Experiences: What “Reframing Risk” Looks Like in Real Life (Illustrative Stories)

Risk has a branding problem. Say the word and people picture skydiving, stock market charts that look like a heart monitor,

or an email from IT that starts with “URGENT” and ends with “mandatory training.” But most of the “risk” you deal with

daily isn’t dramaticit’s quiet, cumulative, and oddly persuasive. It’s the extra mile you drive to avoid traffic (and the

new intersection you’ve never noticed), the “I’ll start tomorrow” you repeat for six months, and the password you reuse

because you’re pretty sure hackers have bigger fish to fry.

Here’s the reframing: risk isn’t a personality trait (“I’m a risk-taker”), and it’s not a moral scorecard (“safe” versus

“reckless”). Risk is information. It’s a relationship between what could happen, how likely it is,

and how much it would matterin a specific context. Once you treat risk as something you can measure, shape,

and communicate, you stop reacting to it like a fire alarm and start using it like a dashboard.

Why We Misunderstand Risk (Even When We’re Sure We Don’t)

Humans are excellent at surviving and only moderately talented at statistics. That’s not an insultit’s an origin story.

Your brain evolved to make fast calls with incomplete data (“Is that rustle a predator?”), not to calculate probabilities

on a spreadsheet while sipping a latte.

Hazard vs. Risk: Same Neighborhood, Different Address

A hazard is something with the potential to cause harm. Risk is the probability that harm will occur

under specific exposure conditions. This distinction matters because it changes the question from “Is this dangerous?”

to “How, when, and to whom could this become dangerous?”

Example: A bottle of bleach has hazardous properties. But the risk depends on how it’s stored, used, and ventilated.

A hazard can be constant while risk varies wildly with behavior and environment. In plain English: the shark is the hazard;

swimming at dusk with a shiny necklace is the risk.

Risk Is a Recipe: Hazard + Exposure + Consequences

Risk tends to get clearer when you break it into ingredients:

hazard (what can cause harm), exposure (how much contact you have with it),

and impact (how bad it would be). You reduce risk by changing any of those ingredients:

remove the hazard, reduce exposure, or reduce the consequences.

Two Lenses for Risk: Numbers and Narratives

Most debates about risk are secretly debates about which lens to use. One person is using the “numbers lens”

(probability and impact), while the other is using the “narratives lens” (emotion, experience, and trust). Both matter.

Ignoring either one is how smart people make painfully avoidable mistakes.

The Numbers Lens: Probability × Impact (Plus a Side of Uncertainty)

In many professional settingscybersecurity, workplace safety, financerisk is often framed as the combination of

likelihood and impact. That’s the core logic behind most risk management approaches:

identify what could go wrong, estimate how likely it is, estimate how damaging it would be, then decide what to do.

The honest twist: uncertainty is always in the room. You rarely know exact probabilities, and impacts can be fuzzy

(financial costs, reputational damage, opportunity loss). So risk management becomes less like predicting the future

and more like making good decisions despite not owning a time machine.

The Narratives Lens: Why “Feels Risky” Can Beat “Is Risky”

Your brain uses mental shortcutsheuristicsto judge risk quickly. They’re useful, but they’re also the reason your

friend refuses to fly (“Planes crash!”) while texting on the highway (“I’m careful!”).

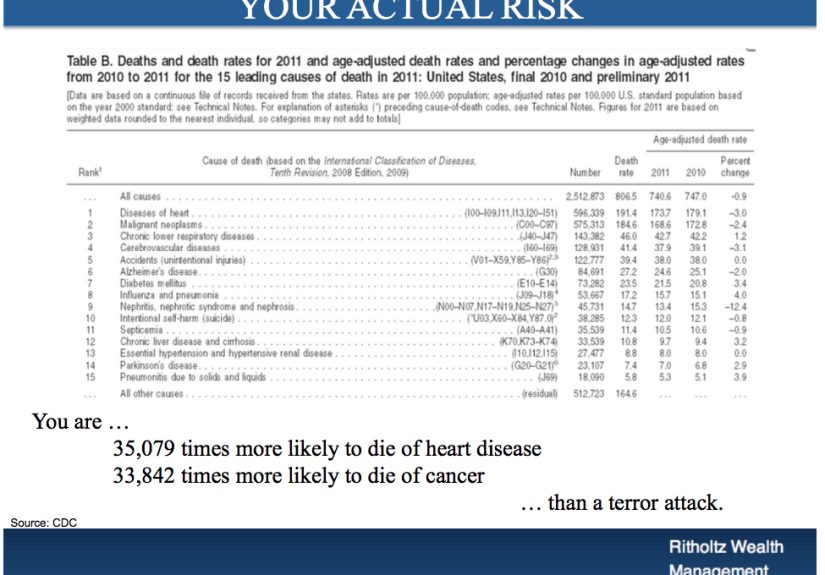

A classic example is availability bias: you judge how likely something is by how easily examples come to mind.

If you just watched a dramatic news story, the event feels more probable, even if the base rate didn’t change.

Another is anchoring: the first number you hear can pull your judgment toward it, even if it’s irrelevant.

The outcome? Risk becomes a popularity contest for vivid stories.

Prospect Theory: Why Losses Feel Like They Use ALL CAPS

One of the most helpful reframes comes from behavioral decision research: people don’t experience outcomes in absolute

terms. We experience them relative to a reference pointwhere we think we “should” beand we tend to feel losses more

intensely than equivalent gains. That’s why a $100 fee can ruin your day while a $100 discount barely gets a nod.

Risk Isn’t Just RiskIt’s Gains vs. Losses in Disguise

Suppose you’re choosing between two options:

- Option A: a guaranteed smaller gain

- Option B: a chance at a bigger gain, but also a chance at getting nothing

Many people become risk-averse with gains (“I’ll take the sure thing”). Now flip it:

- Option C: a guaranteed smaller loss

- Option D: a gamble that could avoid the loss entirely, but could also make it worse

Suddenly, people often become more risk-seekingbecause they’re trying to escape the pain of a sure loss. This doesn’t

mean humans are irrational. It means humans are consistent in a way that spreadsheets don’t predict unless you account

for psychology.

Reframe #1: Risk as a Design Problem (Not a Bravery Test)

If risk is a relationship between likelihood and impact, then managing risk is a form of design. You’re designing

conditions where bad outcomes are less likely, less severe, or easier to recover from.

Three Levers You Can Pull

- Reduce likelihood: prevent the adverse event from happening.

- Reduce impact: limit damage if it happens.

- Increase resilience: recover faster and learn so the next hit hurts less.

This is why seatbelts (impact reduction) and smoke alarms (early detection) coexist with safer building codes

(likelihood reduction). It’s also why cybersecurity isn’t just “block attacks”it’s backups, monitoring, incident

response, and training. Risk becomes manageable when you stop asking “How do I eliminate it?” and start asking

“Where do I want it to land?”

Reframe #2: Risk as a Portfolio (Diversify Your Life, Not Just Your Money)

The investing world has been yelling one message for decades, and it’s surprisingly useful outside finance:

don’t put all your eggs in one basket. Diversification is a way to reduce the chance that one failure

wipes you out. In investing, you spread exposure across assets. In life, you spread exposure across options.

Finance Makes This Obvious: Risk and Return Travel Together

Higher potential returns generally come with higher risk. That doesn’t mean “avoid risk.” It means “choose risk on

purpose.” Investors think about time horizon, diversification, and their ability to tolerate losses. The same logic

applies to career moves, business bets, and personal goals.

Life Portfolios: Practical Examples

-

Career: Build a skills portfolio. If your entire value depends on one tool, one platform, or one client,

your “single point of failure” is wearing a name tag. -

Health: Don’t rely on one heroic habit. A portfolio approach means sleep, movement, nutrition, and stress

managementnot one month of kale and then back to chaos. -

Relationships: Support networks reduce impact when life does its thing. You don’t need 400 acquaintances;

you need a few people who will answer the phone.

Reframe #3: Risk as a Conversation (Because People Don’t Follow Spreadsheets)

Risk communication isn’t “dump data and hope for the best.” It’s guiding people to understand what’s happening,

what’s uncertain, and what actions make sense. In public health emergencies, communication frameworks emphasize

clarity, credibility, empathy, and actionable stepsbecause fear loves ambiguity.

What Great Risk Communication Does

- Builds trust: people act on messages they believe.

- Explains uncertainty: “Here’s what we know, here’s what we don’t, and here’s what we’re doing.”

- Promotes action: specific steps beat vague warnings.

- Respects emotions: feelings aren’t “noise”they’re part of the signal.

Whether you’re talking to customers about a service outage, to employees about policy changes, or to your family about

health choices, the goal isn’t to “win.” It’s to align on reality and next steps.

A 10-Minute Risk Reframe You Can Use Today

Here’s a quick, practical workflow. No jargon, no 47-tab spreadsheet, no “synergy.”

Step 1: Name the Decision (Not the Fear)

“Should we launch this feature next week?” is better than “What if something goes wrong?” because something always can.

Step 2: Separate Hazards from Exposure

List the hazards (what could cause harm) and then the exposure pathways (how you’d actually be affected). This prevents

“it’s dangerous!” from becoming the end of the conversation.

Step 3: Estimate Likelihood and Impact (Roughly Is Fine)

Use ranges if you need to: low/medium/high. Be explicit about assumptions. If you’re guessing, say you’re guessing.

That one movehonestyreduces fake certainty, which is its own kind of risk.

Step 4: Choose One Lever to Pull First

- If likelihood is high: prevent.

- If impact is catastrophic: contain.

- If uncertainty is high: monitor and create rapid response.

Step 5: Make the “Regret Test” Your Tie-Breaker

Ask: “If the bad outcome happens, what will we wish we had done?” That’s your next mitigation. It’s basically a

grown-up pre-mortem, minus the melodrama.

Common Risk Traps (and the Antidotes)

Trap: Confusing Familiar with Safe

Just because you’ve done it 100 times doesn’t mean it’s low risk. It means you’ve gotten away with it 100 times.

Antidote: look for near-misses and weak signals, not just disasters.

Trap: Overweighting Rare but Vivid Events

Plane crashes are vivid. High blood pressure is boring. Guess which one people fear more.

Antidote: check base rates and focus on controllable exposures.

Trap: Underestimating “Slow Risks”

Many of the biggest risks aren’t explosive; they’re erosiveburnout, technical debt, chronic inflammation, fragile

relationships. Antidote: track trends, not just incidents.

Trap: Treating Risk as “All or Nothing”

If the only options are “perfect safety” or “YOLO,” you’ll make worse choices.

Antidote: design partial protections, staged rollouts, pilots, and exit ramps.

Conclusion: The Point Isn’t Less RiskIt’s Better Risk

Reframing risk doesn’t make you fearless. It makes you accurate. And accuracy is underrated.

When you separate hazards from exposure, balance numbers with narratives, and design mitigations like an engineer of

your own outcomes, risk stops being a vague threat and becomes a tool.

The goal is not to eliminate uncertainty. The goal is to stop being surprised by the same kinds of problems, to spend

your courage where it matters, and to build systemsfinancial, professional, personalthat can take a hit without

falling apart. In other words: risk isn’t the villain. Unexamined risk is.

Experiences: What “Reframing Risk” Looks Like in Real Life (Illustrative Stories)

The concept sounds clean on paper: likelihood, impact, mitigation. But real life is messy, emotional, and occasionally

held together with duct tape and calendar reminders. Here are a few illustrative, true-to-life scenarios that show how

reframing risk changes decisions. Think of them as “experience patterns” you might recognize from work, family, or the

group chat where someone always says, “It’s probably fine.”

1) The Startup Launch That Didn’t Need BraveryIt Needed Guardrails

A small team is preparing to launch a new feature. The debate gets dramatic fast: one side says delaying is “playing

scared,” the other side says launching is “reckless.” That framing turns risk into a character judgment.

The reframe is simple: what are the most plausible failure modes, and which ones are catastrophic?

They identify three: (a) a payment bug that charges people incorrectly (high impact), (b) a performance slowdown

(medium impact), and (c) a confusing UI that increases support tickets (annoying, but survivable). Instead of arguing

about courage, they design responses: a staged rollout, extra monitoring, and a quick rollback plan. The launch happens

on time, not because they ignored risk, but because they gave it a safe place to land. The team feels calmer because

they’re not relying on luck as their primary strategy.

2) The “I’m Careful” Ladder Moment

Someone decides to clean gutters. They’ve done it before, so it feels safe. Familiarity is comfortingand sneaky.

The hazard (falling) hasn’t changed. Exposure has: it’s windy, the ground is damp, and the ladder is set at a worse

angle because the hose is in the way.

Reframing risk means asking, “What’s the exposure pathway?” In this case: slippery shoes + unstable base + height.

The mitigation isn’t heroism. It’s boring excellence: stabilize the ladder, wait for better conditions, use a spotter,

or hire help. In many households, the most effective risk management tool is not a spreadsheetit’s a second adult

saying, “Please don’t make me explain to the ER doctor that this was for ‘quick cleaning.’”

3) The Investment Panic and the Portfolio Perspective

Markets dip. Headlines go full apocalypse. An investor feels the urge to “do something” immediatelyusually the thing

they’ll regret later. This is where reframing risk as a portfolio changes behavior. The question isn’t “Will my

investments ever go down?” (they will). The question is “Is my exposure aligned with my time horizon and tolerance for

volatility?”

Instead of selling everything in a panic, they zoom out: diversification, asset allocation, and emergency savings are

impact reducers. They rebalance calmly or do nothingbecause sometimes the best action is refusing to let your emotions

drive the car. The reframe turns volatility from “danger” into “expected weather,” and the plan becomes an umbrella,

not a tantrum.

4) The Health Scare That Was Actually a Systems Issue

A person gets a concerning lab result and spirals into doom-scrolling. The fear is real, but the risk conversation is

incomplete. Reframing starts with separating hazard from exposure: what is the actual condition, what factors increase

likelihood, and what changes reduce exposure over time?

Many health risks aren’t solved by one dramatic intervention. They’re managed by systems: medication adherence,

consistent sleep, regular movement, follow-ups, and reducing the “slow risks” like chronic stress. The reframe shifts

the mindset from “I’m doomed” to “I have levers.” That shift doesn’t guarantee outcomes, but it restores agencyand

agency is one of the best antidotes to panic.

5) The Family Argument That Was Really About Trust

Two relatives argue about a safety decision. One cites statistics, the other cites a scary story they heard. Both feel

unheard. Reframing risk as a conversation means addressing the emotional layer without abandoning facts. A productive

approach sounds like: “I get why that story stuck with you. Here’s what we know is common, here’s what’s rare, and here

are the steps that reduce risk either way.”

When the conversation includes empathy and actionrather than dunking on each other’s intelligencepeople move from

defensiveness to decisions. The reframe turns conflict into collaboration: not “Who’s right?” but “What’s a reasonable

plan we can live with?”

In every scenario, reframing risk doesn’t eliminate uncertainty. It turns uncertainty into something you can work with:

assumptions you can test, exposures you can reduce, and impacts you can cushion. That’s the winless drama, better

decisions, and fewer moments where “probably fine” becomes a headline.