Table of Contents >> Show >> Hide

- What “Animal Spirits” Really Means (and Why It’s Not a Zoo Metaphor)

- The “Money Tree” Fantasy: A Shortcut That Feels Like a Strategy

- What the “Money Tree” Episode Captures About Modern Markets

- Guardrails: How to Keep a Hot Story From Hijacking Your Plan

- Specific Examples of the Money Tree Mindset (and Better Alternatives)

- So… Is There a Money Tree?

- Experiences Related to “Money Tree” That Investors Commonly Describe

If you’ve ever looked at your brokerage app, your credit card bill, and your neighbor’s brand-new “investment” boat and thought,

“Cool… where do I get one of those money trees?”welcome. You’re not alone, you’re not broken, and you’re definitely not the only person

who’s noticed that “financial success” can look suspiciously like a magic trick when you only see the highlight reel.

In the Animal Spirits episode titled “Money Tree” (hosted by Ben Carlson of A Wealth of Common Sense and Michael Batnick),

the conversation bounces through a familiar modern investing landscape: crypto on corporate balance sheets, larger-than-life CEOs,

the feeling that markets are “rigged,” and the temptation to treat home equity like an ATM that politely refuses to say “no.”

Underneath the jokes and rapid-fire topics is a serious point: most bad financial decisions don’t start as “bad.” They start as “obvious.”

This article unpacks the “money tree” mindsetwhy it shows up, how it messes with our decisions, and how to build guardrails that keep your

financial plan from getting yeeted off a cliff by a single hot narrative. We’ll keep it practical, a little funny, and very grounded in how money

tends to behave in real life: slowly, then suddenly, then slowly again.

What “Animal Spirits” Really Means (and Why It’s Not a Zoo Metaphor)

The phrase “animal spirits” goes back to economist John Maynard Keynes, who used it to describe the emotional and psychological forces that

drive economic decisionsespecially under uncertainty. In plain English: people don’t invest like robots. They invest like humans… which means

confidence, fear, envy, tribalism, and storytelling all get a seat at the table.

That’s not a moral failure; it’s a design spec. Markets are giant voting machines for narratives in the short run and messy weighing machines in the

long run. The problem isn’t having emotionsit’s pretending you don’t. That’s like saying you’ll “only eat healthy” while living inside a donut shop.

The “Money Tree” Fantasy: A Shortcut That Feels Like a Strategy

A “money tree” is the belief (sometimes loud, sometimes subtle) that there’s a dependable shortcut to wealth: the one weird trick, the secret asset,

the perfect trade, the “everyone else is doing it” opportunity that turns ordinary savings into extraordinary outcomesfast.

Why the money tree story is so seductive

- It turns uncertainty into certainty. You don’t have to wonder what to do; you just do the thing.

- It promises identity. You’re not “a person saving steadily.” You’re “an early adopter.” A “market wizard.” A “visionary.”

- It offers emotional relief. If you feel behind, the shortcut feels like justicenot risk.

- It’s social-media friendly. “I diversified and rebalanced” gets zero likes. “This trade paid my rent” gets a documentary deal.

The reality: wealth usually comes from boring behaviors repeated for a long timespending less than you earn, investing consistently, avoiding

catastrophic errors, and letting compounding do its slow, unglamorous work. The money tree fantasy isn’t wrong because big wins never happen.

It’s wrong because it teaches you to expect big wins as the baselineand that expectation quietly changes how you take risk.

What the “Money Tree” Episode Captures About Modern Markets

The episode’s topic list reads like a time capsule of what gets investors fired up: corporate bitcoin headlines, CEO mythology,

big-tech dominance, the Robinhood era, and the persistent sense that the system favors insiders. Let’s pull out a few themes and translate them

into “what to do with your actual money.”

1) Personal finance is still the main character

Markets are interesting. Personal finance is consequential. One of the smartest subtexts in “Money Tree” is the reminder that

financial literacy isn’t a side quest. If you don’t understand interest rates, taxes, credit, diversification, and risk, you’re basically

bringing a pool noodle to a sword fight.

Here’s a not-sexy but powerful example: many households can’t comfortably absorb a surprise expense or a period of lost income. That’s not a judgment;

it’s an incentive structure. When your financial cushion is thin, the money tree fantasy becomes more tempting because slow-and-steady feels like a luxury.

The antidote is not “be perfect.” It’s build the basics first: emergency savings, high-interest debt management, and a plan for retirement contributions.

2) CEO mythology can turn into market mythology

When markets get frothy, we start treating CEOs like comic-book characters. The “golden touch” narrativewho’s the next Buffett, who belongs on the

CEO Mount Rushmorecan subtly turn into an investing strategy: buy what the genius touches.

The catch is that “great leader” and “great investment at this price” are not the same sentence. Even legendary businesses can be mediocre investments

when expectations get unrealistic. The most common investing error here isn’t buying a great companyit’s paying a price that assumes perfection,

then acting surprised when reality shows up in sweatpants.

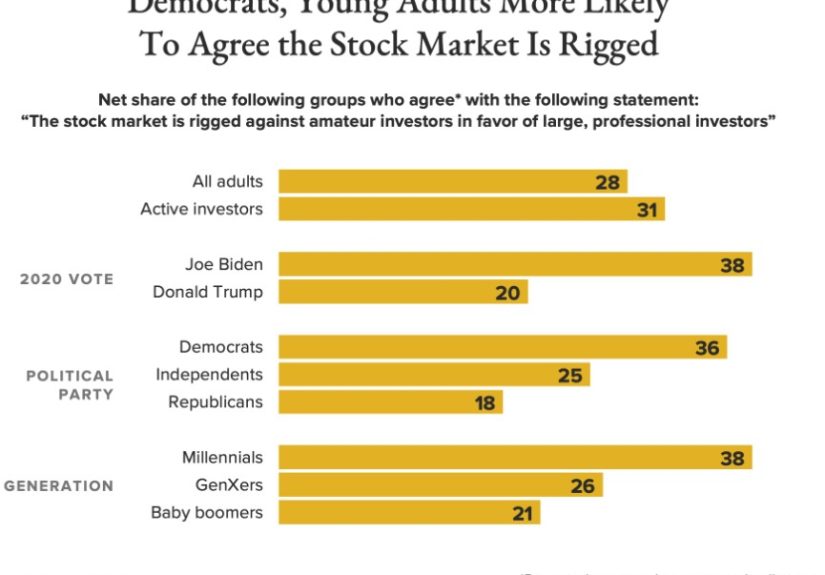

3) “The market is rigged” is a feeling… and sometimes a catalyst

The episode raises the question: why do so many people feel the market is rigged against them? That belief can be emotionally rational even when the

underlying mechanics are complicated. Market structure, unequal access, different tax treatments, and “rules that feel different for different people”

create fertile ground for distrust.

But here’s the twist: believing the market is rigged can push investors into even riskier behavior. If you feel you can’t win by “playing fair,”

you may reach for leverage, options, or concentrated bets to “catch up.” That’s not rebellion; it’s self-sabotage with better branding.

4) Robinhood, day trading, and the “frictionless” trap

When trading becomes frictionlessno commissions, instant deposits, confetti animations (RIP), infinite scroll of hot tickersthe brain treats investing

like entertainment. The “biggest hurdle for day traders” is rarely intelligence. It’s behavior: overtrading, chasing volatility, and confusing activity

with progress.

Guardrail idea: create a bright line between investing (goal-based, long-term, diversified) and speculating (short-term,

high-variance, entertainment-adjacent). If you insist on speculating, do it with a small, pre-set “tuition budget” and keep it quarantined from the money

you actually need for life.

5) The “money tree” shows up in leverage: margin and home equity

Two of the most tempting “money tree” tools are also the most unforgiving: margin (borrowing against your portfolio) and

home equity (borrowing against your house).

Margin can magnify gains, but it also magnifies losses and can trigger forced selling at the worst possible time. Home equity lines of credit can feel

flexible, but variable rates and changing terms can turn “cheap money” into “why is my payment doing parkour?” Borrowing can be useful,

but it demands humilitybecause debt doesn’t care about your narrative.

Guardrails: How to Keep a Hot Story From Hijacking Your Plan

“Putting guardrails on your investments” is one of the most practical ideas tied to this episode. Guardrails are not about avoiding risk.

They’re about avoiding unplanned risk.

Guardrail #1: Write down your “rules of engagement” when you’re calm

You want your portfolio decisions to be made by the version of you who is hydrated, well-rested, and not doom-scrolling market headlines at 1:12 a.m.

A simple one-page investing policy can include:

- Your target stock/bond allocation

- Your rebalancing schedule (calendar-based or threshold-based)

- What would actually make you change the plan (job loss, retirement date change, major life event)

- What will not make you change the plan (a scary headline, a friend’s hot tip, a trending ticker)

Guardrail #2: Protect your “time in the market” from your emotions

Many investors don’t lose money because the market failsthey lose money because they repeatedly exit and re-enter at the wrong times.

It’s not that timing is impossible once. It’s that timing is hard to do consistently, especially when volatility clusters and headlines get dramatic.

A simple behavior upgrade: automate contributions (401(k), IRA, brokerage), then treat investing like brushing your teethnon-negotiable, not mood-based.

You can still rebalance and adjust, but the default is “keep going.”

Guardrail #3: Diversify your information diet

People often say, “diversify your portfolio.” Great. Also diversify your inputs. If your feed is all memes, hype, and outrage, your portfolio will start to

resemble a dare. Mix in boring, evidence-based sources and long-term perspectives. Your future self will thank you with a polite nod and better returns.

Guardrail #4: Use “friction” on purpose

Modern finance removes friction. You can add it back:

- Require a 24-hour waiting period before any new single-stock buy

- Disable options approval unless you have a defined use case

- Move “fun money” to a separate account with a fixed cap

- Unfollow accounts that turn investing into a personality contest

Specific Examples of the Money Tree Mindset (and Better Alternatives)

Example 1: “If Tesla bought bitcoin, it must be smart.”

Corporate actions can validate a trend, but they don’t eliminate risk. A better approach is to ask:

What role would this asset play in my plan? If the answer is “I don’t know, but it’s going up,” that’s not a role. That’s a vibe.

Vibes are not tax-advantaged.

Example 2: “The market is rigged, so I need leverage to catch up.”

Leverage is not a catch-up tool. It’s a fragility tool. If your plan requires leverage to succeed, your plan has a structural problem.

A better alternative: increase your savings rate, invest in diversified funds, and extend your time horizon. “Catch up” is usually a math problem,

not a cleverness problem.

Example 3: “I’ll just tap home equitymy house is basically an investment account.”

Home equity can be a resource, but it’s not a free resource. The better alternative is to treat it like a last-mile tool:

useful for strategic renovations, debt consolidation under strict conditions, or planned needsnot as a routine funding source for lifestyle creep.

So… Is There a Money Tree?

Kind of. It’s just not the one people want. The real money tree is:

steady saving + diversified investing + time + avoiding big mistakes.

It’s not flashy, but it works often enough that it’s basically the closest thing finance has to cheatinglegally.

The “Money Tree” episode is a reminder that markets are never just numbers. They’re stories. And stories can be usefuluntil they become a substitute

for a plan. The goal isn’t to ignore animal spirits. The goal is to acknowledge them, laugh at them a little, and then

build a system that doesn’t depend on perfect self-control.

Experiences Related to “Money Tree” That Investors Commonly Describe

I don’t have personal investing memories (no childhood lemonade stand portfolio here), but there are patterns and “you could’ve written this yourself”

experiences that show up again and again when people talk about money, markets, and the urge to find a shortcut. If you recognize yourself in any of

these, congratulations: you are a normal human being living in a very persuasive financial era.

1) The screenshot season

Someone in a group chat posts a screenshot of a one-week gain that looks like a typo. The vibe is pure electricity: rocket emojis, “I told you,”

and a casual suggestion that you’re missing the easiest money of all time. A lot of people describe the same emotional sequence:

curiosity → urgency → mild shame → purchase. Not because the investment thesis is airtight, but because the social proof feels airtight.

The healthier version of this experience is learning to pause and ask: “If this goes to zero, what changes about my life?” If the answer is

“everything,” it’s too big. If the answer is “annoying but fine,” it might be contained speculation. The money tree fantasy thrives when the position size

is driven by emotion instead of planning.

2) The “rigged” spiral

People often describe a moment where the market feels personal: a sudden drop right after they invest, a trading halt they don’t understand, or a news

cycle that sounds like it was written to humiliate retail investors. That’s when “the market is rigged” shifts from an opinion to an identity.

And identity-level beliefs are powerfulthey can push you toward risky “revenge trades” designed to reclaim dignity, not build wealth.

A useful counter-experience is building a simple, boring benchmark for success: “Did I contribute this month? Did I rebalance when needed?

Did I avoid taking on debt for a gamble?” Those are wins you control. They also quietly turn down the volume on the rigged narrative, because

your progress becomes less dependent on the day-to-day drama.

3) The leverage “confidence boost” that fades fast

Another common story: someone tries margin or short-dated options for the first time, sees a quick win, and suddenly feels “smarter.”

Leverage has a way of converting luck into confidence at record speed. Then comes the second phase: volatility. The position swings harder than expected,

stress increases, and decision-making gets reactive. People describe checking prices constantly, sleeping worse, and feeling trappedbecause exiting now

would “make it real.”

The better lesson many people eventually take away is that leverage is a tool for very specific, well-modeled use casesnot a default accelerator for

wealth-building. If you don’t have a written plan for how leverage fits, it usually doesn’t fit.

4) The home equity temptation

When home prices rise, homeowners often describe a strange emotional shift: they feel wealthier, even if their monthly budget hasn’t changed at all.

That can make tapping equity feel reasonable, even “responsible”especially when the spending is framed as investment: renovations, education,

or consolidating debt. But the line between “strategic” and “justified” can get blurry.

A common turning point is realizing that debt is still debt, even when it’s backed by something that went up in value. People often describe the relief of

setting a rule like: “Home equity is not for funding lifestyle. It’s for defined needs with a payoff plan.” That one sentence can save years of stress.

5) The calm that comes from guardrails

The most positive experience people describe is surprisingly simple: once they automate investing, keep a cushion, and set rules, they feel less

emotionally reactive. They still notice headlines, but they’re less likely to act on them. The market becomes something they participate in,

not something that controls their mood. That’s not just good for returnsit’s good for life.

If the “money tree” is the fantasy of effortless wealth, guardrails are the reality of effortless consistency. And consistency, over time,

is what starts to look like magic.