Table of Contents >> Show >> Hide

- Quick Map: What You’ll Learn

- Episode 39’s Big Backdrop: Markets Are Built on a Few Big Winners

- The Worst 401(k) Advice (and Why It’s So Popular)

- 1) “Skip the 401(k) until you’re making more money.”

- 2) “Only contribute up to the match. Anything beyond that is optional.”

- 3) “When the market drops, move to cash until things feel safer.”

- 4) “Fees don’t matter that muchfocus on performance.”

- 5) “Put most of your 401(k) in company stockit shows confidence.”

- 6) “Borrow from your 401(k). You’re paying yourself back, so it’s basically free.”

- 7) “Cashing out your 401(k) when you leave a job is no big deal.”

- Contribution Limits: The “Speed Limit” of Tax-Advantaged Saving

- How Hard Is It to Become a 401(k) Millionaire?

- Fund Choice Without the Headache: A Simple Decision Framework

- Rollovers, Job Changes, and the “Don’t Accidentally Blow It Up” Checklist

- What Episode 39 Gets Right: Behavior Beats Brilliance

- Conclusion: The Best 401(k) Strategy Is the One You’ll Actually Follow

- Experience Section: of “This Is How Bad 401(k) Advice Usually Plays Out”

If your 401(k) could talk, it would say: “Please stop treating me like a checking account with a retirement cosplay outfit.” In Animal Spirits Episode 39 (aired in 2018), hosts Michael Batnick and Ben Carlson riff on markets, concentration, and the kind of 401(k) “wisdom” that sounds confidentright up until you do the math.

This article takes the spirit of that episode and builds a practical, modern guide around it: what the worst 401(k) advice looks like in the wild, why it’s so tempting, and what to do insteadwithout turning your retirement plan into a reality TV show. (Spoiler: the market already provides enough drama. You don’t need to add plot twists.)

Quick Map: What You’ll Learn

- How Episode 39 connects stock market “winner concentration” to why diversification matters in a 401(k)

- The most common “Worst 401(k) Advice” greatest hitsand why they backfire

- Contribution limits (including 2026 numbers) and how to use them wisely

- Fees, fund choices, and why “small” percentages aren’t small over decades

- Rollovers, cash-outs, and loans: how good intentions turn into expensive mistakes

- A 500-word experience section at the end with real-world-style scenarios and lessons

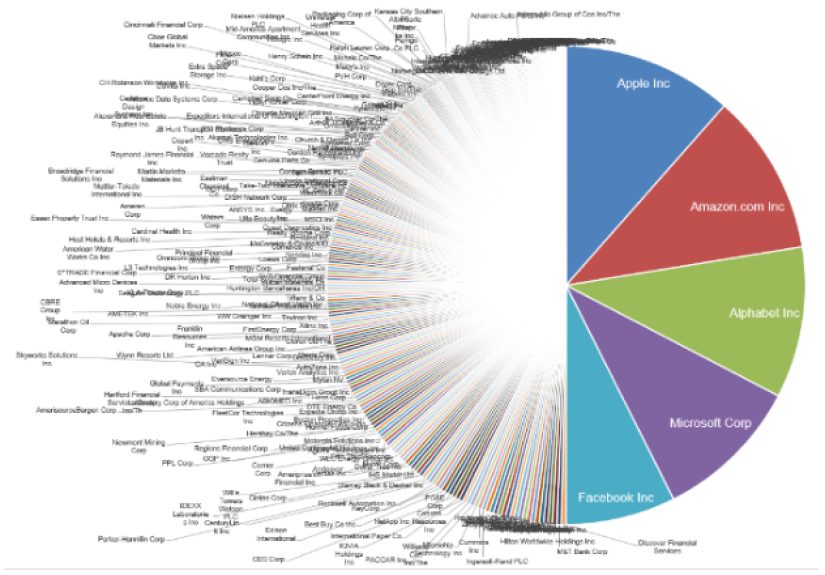

Episode 39’s Big Backdrop: Markets Are Built on a Few Big Winners

One of the episode’s themes is the idea that markets often look “unfair” because returns are lopsided. A relatively small group of stocks tends to drive a huge share of long-term wealth creation. That’s not a bugit’s a feature. It’s the market’s version of “a few people eat most of the nachos.”

Here’s why that matters for your 401(k): if you try to hand-pick winners, you’re betting you can identify the tiny group that carries the whole team. But if you own a broad index (or a diversified target-date fund), you’re more likely to capture those winners without needing a crystal ballor a cousin who “has a feeling about tech.”

Episode 39 also pokes at “pie chart panic”those viral charts showing the market dominated by a handful of mega-companies. The easy takeaway is: “That’s scary, I should do something.” The better takeaway is: “That’s exactly why broad diversification exists.” If gains are concentrated, owning the market beats trying to guess which slice gets bigger next.

The Worst 401(k) Advice (and Why It’s So Popular)

Bad 401(k) advice spreads because it’s emotionally satisfying. It makes you feel in control. And it often contains a tiny seed of truth that gets stretched into a full-blown myth. Let’s de-myth the classics.

1) “Skip the 401(k) until you’re making more money.”

Translation: “Delay compounding, ignore free employer match dollars, and rely on your future self to be more disciplined than your current self.” If your employer matches contributions, skipping the plan can mean turning down part of your compensation.

A better approach: contribute at least enough to capture the full employer match (if offered), then scale up as income grows. Starting small beats starting “someday.”

2) “Only contribute up to the match. Anything beyond that is optional.”

The match is a great first target, but stopping there can leave you under-savingespecially if you started late or want a bigger cushion. For many households, the match is the appetizer, not the meal.

Better approach: treat the match as the minimum win, not the finish line. If you can, use automatic escalation (e.g., +1% per year) so your savings rate climbs without you having to “feel motivated” every January.

3) “When the market drops, move to cash until things feel safer.”

This is how people accidentally buy high and sell low while believing they’re being “careful.” If your time horizon is years (or decades), volatility is part of the price of admission. Panic-selling inside a retirement plan can turn temporary declines into permanent damage.

Better approach: pick an asset allocation you can stick with. If you want a set-it-and-forget-it option, a target-date fund may be appropriate for many savers because it automatically rebalances and gradually becomes more conservative over time.

4) “Fees don’t matter that muchfocus on performance.”

Fees matter precisely because they’re boring. They show up quietly, every year, forever. Even small differences compoundmeaning high fees can quietly eat a meaningful chunk of your lifetime returns.

Better approach: compare expense ratios (and any plan administrative fees) as part of your decision. Low-cost index funds and competitively priced target-date funds often provide a strong baseline. You don’t have to be cheap about everything in life. But your retirement plan is a pretty good place to practice.

5) “Put most of your 401(k) in company stockit shows confidence.”

Confidence is great. Concentrating your retirement in the same place you get your paycheck is less great. If your employer hits trouble, you can face a double-whammy: job loss and portfolio loss at the same time.

Better approach: diversify. If company stock is part of the plan (or an ESPP is involved), consider setting a sensible cap so one company doesn’t dominate your retirement future.

6) “Borrow from your 401(k). You’re paying yourself back, so it’s basically free.”

401(k) loans can be useful in true emergencies if the plan allows them and you understand the trade-offs. But “basically free” is a fantasy. While money is out of the market, you can miss potential growth. And if you leave your job, repayment rules can get urgentturning a loan into taxes and penalties if it defaults.

Better approach: treat loans as last-resort tools, not lifestyle financing. If you must borrow, read your plan’s rules carefully and understand repayment requirementsespecially if you might change jobs.

7) “Cashing out your 401(k) when you leave a job is no big deal.”

This might be the heavyweight champ of bad 401(k) advice. Cashing out can trigger income taxes and (in many cases) an additional 10% penalty if you’re under 59½. Worse, you’re ripping up the compounding engine just when it’s starting to warm up.

Better approach: consider a direct rollover to an IRA or your new employer plan (if allowed), or keep it in the old plan if the fees and investment options are solid. The goal is to keep the money workingnot hand it over to taxes and penalties because “moving is annoying.”

Contribution Limits: The “Speed Limit” of Tax-Advantaged Saving

A 401(k) is powerful partly because it’s tax-advantagedbut it comes with annual contribution limits. Knowing the limits helps you plan, especially if you’re trying to catch up later or you’ve got variable income.

2026 headline numbers (common scenarios)

- Employee elective deferral limit: $24,500

- Catch-up (age 50+ in most plans): +$8,000 (total often up to $32,500)

- Higher catch-up (ages 60–63, where applicable): potentially higher than the standard catch-up

These limits can change over time, and your plan’s rules matter (for example, which contributions are pre-tax vs Roth, and any employer match formula). The key behavioral takeaway: if you get a raise, bonus, or finish paying off a big bill, increasing your contribution rate is one of the cleanest ways to turn “extra money” into “future freedom.”

How Hard Is It to Become a 401(k) Millionaire?

Episode 39 touches on the “401(k) millionaire” ideathe financial equivalent of spotting a unicorn at Target. It’s absolutely possible, but it’s usually not the result of one genius trade. It’s boring consistency, decent savings rates, and time.

Illustrative examples (not guarantees, just math)

Scenario A: Starting salary $70,000. Total contributions (employee + employer) = 14%. Salary grows 3% annually. Portfolio returns average 7% annually. Time horizon: 40 years.

Result: roughly $3.0 million by year 40 (ballpark).

Scenario B: Same inputs, but you start 10 years later (30 years instead of 40).

Result: roughly $1.3 million (ballpark).

That gap isn’t because the late starter is “bad at money.” It’s because compounding is basically a snowball that needs a hill. Time is the hill. Starting earlier gives the snowball more runway.

Fund Choice Without the Headache: A Simple Decision Framework

Most 401(k) plans offer a menu: index funds, actively managed funds, bond funds, maybe a stable value fund, and often target-date funds. The “worst advice” angle shows up when people either overcomplicate everything or ignore everything. Let’s aim for the middle: simple, intentional, and maintainable.

Step 1: Pick your approach

- Hands-off approach: A single target-date fund aligned with your expected retirement year can be a practical choice for many savers. It auto-diversifies and auto-rebalances.

- Hands-on approach: Build a diversified mix (e.g., U.S. stocks, international stocks, bonds) and rebalance occasionally. Keep it simple enough that you’ll actually stick to it.

Step 2: Check fees and plan costs

If two funds do roughly the same job, the cheaper one often has an edge over long periods. You don’t need to obsess over one basis point, but you should care about the difference between “low-cost” and “quietly expensive.”

Step 3: Set a contribution plan that survives real life

The best savings rate is the one you can maintain across boring months, stressful months, and “why is my car making that sound?” months. Auto-escalation and automatic contributions help you keep going when motivation disappearswhich, to be clear, is most of the time.

Rollovers, Job Changes, and the “Don’t Accidentally Blow It Up” Checklist

Job changes are where good savers make expensive mistakesnot because they’re reckless, but because the process feels administrative, and admin tasks are where dreams go to nap.

If you leave a job, consider these moves (in this order)

- Don’t cash out unless it’s truly unavoidable. Taxes + potential penalty + lost growth is a brutal combo.

- Check fees and fund options in the old plan. Sometimes keeping it there is perfectly fine.

- Consider a direct rollover to an IRA or your new employer plan (if allowed) to keep taxes simple.

- If you have a 401(k) loan, learn the repayment timeline before you resign. This is not a fun surprise.

Also, beware of “helpful” rollover pitches that sound like a universal upgrade. Sometimes a rollover is beneficial. Sometimes the old plan is cheaper and better. The right answer depends on fees, investment options, services, and your own behavior.

What Episode 39 Gets Right: Behavior Beats Brilliance

The punchline of most 401(k) horror stories isn’t “bad markets.” It’s “bad decisions in response to markets.” Episode 39’s broader pointwoven through market concentration talk, factor debates, and cultural noiseis that investing success is usually the result of doing a few things consistently and avoiding the big self-inflicted wounds.

The “Anti-Worst-Advice” 401(k) Playbook

- Get the match if offered. It’s part of your pay.

- Increase contributions as income risesautomate it if possible.

- Use diversified, low-cost options (index funds or target-date funds are common building blocks).

- Ignore the urge to time the market inside your retirement plan.

- Don’t cash out when changing jobs unless you’ve exhausted alternatives.

- Respect fees and avoid expensive complexity you can’t explain in one sentence.

- Keep it boringbecause boring is how retirement gets funded.

Conclusion: The Best 401(k) Strategy Is the One You’ll Actually Follow

Animal Spirits Episode 39 is fun because it treats finance the way it shows up in real life: messy, emotional, and occasionally ridiculous. The “worst 401(k) advice” theme lands because it’s so relatablemost of us have heard at least one of these myths from a well-meaning coworker, a loud relative, or the internet comment section (humanity’s greatest laboratory for bad ideas).

The good news is that 401(k) success doesn’t require perfection. It requires avoiding the big traps, keeping costs reasonable, staying diversified, and saving consistently over time. Do that, and you’ll be ahead of most “hot takes”and probably sleeping better, too.

Experience Section: of “This Is How Bad 401(k) Advice Usually Plays Out”

If you spend enough time reading plan disclosures, employer FAQs, provider education pages, and the endless stream of “help, I did a thing” stories people post online, you notice the same patterns repeating like a catchy chorus. Here are a few realistic, composite-style scenarios that capture how the worst 401(k) advice tends to unfoldand what the smarter pivot looks like.

Story #1: The Match Left on the Table

Someone hears: “Investing can wait until your income is higher,” so they contribute 0% for a couple of years. Later they learn their employer matched the first chunk of contributions the whole time. It’s not just missed investment growthit’s missed compensation. The emotional arc is always the same: mild disbelief, followed by “Wait, you’re telling me I got a pay cut because I didn’t fill out a form?” The fix is simple: contribute at least enough to capture the full match, even if you start small. You can always raise the percentage later. You can’t go back in time and retroactively collect match dollars you never claimed.

Story #2: The “Safety Fund” That Became a 12-Year Vacation

Another classic: someone chooses the stable value or money market option because it feels safe, then never revisits the allocation. Years pass. The account grows, but mostly from contributionsnot compounding. When they finally check, they’re confused: “I put in real money. Why doesn’t it look like the market’s been doing?” Because the market did. Their account didn’t. The fix isn’t to swing wildly into risky bets; it’s to pick a diversified allocation aligned with a long time horizon (or use a target-date fund) and periodically confirm it still matches reality. “Set it and forget it” only works if you set it correctly.

Story #3: The Panic Switch

During a scary market drop, someone moves everything to cash “just for now.” Then they wait for things to feel safe again. The problem is that “safe” usually arrives after prices have already rebounded. So they miss the recovery, feel betrayed by investing, and either stay in cash too long or jump back in after confidence returns (often at higher prices). The fix is behavioral: decide your plan during calm weather, not the hurricane. If volatility keeps you awake, adjust your risk level once and stick to itdon’t improvise every time headlines get dramatic.

Story #4: The 401(k) Loan Surprise Ending

Someone borrows from their 401(k) because “I’m paying myself back.” Then they change jobs sooner than expected, and repayment becomes urgent. If the loan defaults or is treated as a distribution, taxes (and possibly penalties) show up like an uninvited guest who also ate your leftovers. The fix: before borrowing, read the plan rules and think through job-change risk. If the loan is truly unavoidable, create a repayment plan that works even if your employment changes.

The shared lesson across all of these: the worst 401(k) advice usually isn’t a single bad decisionit’s a small decision that people never revisit. Good outcomes come from simple systems that survive real life: automate contributions, diversify, keep fees reasonable, and avoid turning normal market movement into a personal emergency.