Table of Contents >> Show >> Hide

- What Is a Pay Check Stub?

- Way 1: Start With Gross Pay, Hours, and Earnings

- Way 2: Review Taxes, Deductions, and Net Pay

- Way 3: Check Year-to-Date Totals and Spot Red Flags

- Sample Pay Stub Walkthrough

- Common Pay Stub Abbreviations

- How Often Should You Review Your Pay Stub?

- Why Reading Your Pay Stub Helps Your Budget

- Experience-Based Tips for Reading a Pay Check Stub

- Conclusion

Note: This article is based on current U.S. payroll, tax withholding, wage-record, and pay-statement information from reputable government, financial education, payroll, and tax resources.

Your paycheck stub may look like it was designed by a committee of accountants, tax attorneys, and someone who really enjoys abbreviations. “FICA,” “YTD,” “MED,” “FIT,” “401(k),” “gross,” “net”it can feel less like a pay record and more like a tiny financial escape room.

But here is the good news: once you know what to look for, learning how to read a pay check stub is not difficult. A pay check stub, also called a pay stub, paycheck stub, wage statement, or earnings statement, explains how your employer calculated your pay for a specific pay period. It shows what you earned, what was deducted, and what actually landed in your bank account. In other words, it tells the story of your paycheck before taxes and deductions marched in wearing sensible shoes.

Reading your pay stub matters because it helps you catch errors, understand your tax withholding, confirm overtime or bonus pay, track retirement contributions, and budget based on real take-home paynot the number you wish you were taking home. Whether you are paid hourly, salaried, by commission, or with a mix of wages and bonuses, your pay stub is one of the most useful financial documents you receive all year.

This guide breaks the process into three practical ways: reading your earnings, reviewing your deductions, and checking your year-to-date totals. By the end, you will know how to read a pay check stub with confidenceand maybe even stop side-eyeing the payroll section like it personally owes you money.

What Is a Pay Check Stub?

A pay check stub is a detailed record of your compensation for a specific pay period. It usually includes your employer’s information, your identifying information, the pay period dates, your gross pay, taxes withheld, benefit deductions, retirement contributions, and your net pay. If you receive direct deposit, your pay stub may be available through an online payroll portal instead of attached to a paper check.

Federal law requires employers to keep accurate payroll records, including wages paid and hours worked. However, federal law does not generally require every employer to give employees a pay stub. Many states do require wage statements, and the exact rules vary. That is why your stub may look different depending on your state, employer, and payroll provider.

Still, most pay stubs follow the same basic structure. Once you understand the core sections, you can read almost any versionfrom a clean digital payroll statement to a paper stub that looks like it escaped from 1998.

Way 1: Start With Gross Pay, Hours, and Earnings

The first way to read a pay check stub is to look at the earnings section. This is where your employer shows how much you earned before anything was taken out. This amount is called gross pay.

Gross Pay: The Big Number Before Reality Arrives

Gross pay is your total earnings for the pay period before taxes, insurance premiums, retirement contributions, garnishments, or other deductions are subtracted. If you are salaried, your gross pay is usually your annual salary divided by the number of pay periods in the year. If you are hourly, it is typically your hourly rate multiplied by the number of hours worked, plus any overtime, holiday pay, bonuses, commissions, or shift differentials.

For example, suppose you earn $25 per hour and worked 80 regular hours during a two-week pay period. Your regular gross pay would be:

$25 × 80 hours = $2,000 gross pay

If you also worked 5 overtime hours at time-and-a-half, your overtime rate would be $37.50 per hour:

$37.50 × 5 overtime hours = $187.50 overtime pay

Your total gross pay for that period would be:

$2,000 + $187.50 = $2,187.50

This is the starting point for your paycheck. It is not your take-home pay. It is the “before the deductions buffet” number.

Hours Worked and Pay Rates

If you are paid hourly, your pay stub should usually show the number of hours worked and the rate used to calculate each type of pay. Common categories include regular hours, overtime hours, holiday pay, paid time off, sick leave, training hours, shift differential, and bonus pay.

This section is important because small errors can become expensive. If you worked 86 hours but your stub shows 80, that is not a tiny typoit is potentially unpaid wages. If your overtime rate is wrong, your take-home pay may be short. Under federal wage rules, many nonexempt employees must receive overtime pay at at least one and one-half times their regular rate for hours worked over 40 in a workweek. Some states have additional overtime rules, so your location may matter.

When reviewing this section, compare your pay stub against your own records. Keep a simple note of your shifts, hours, overtime, and any approved paid time off. You do not need a complex spreadsheet worthy of NASA; even a phone note can help you spot mistakes.

Common Earnings Labels on a Pay Stub

Pay stubs often use short labels. “REG” may mean regular pay. “OT” usually means overtime. “HOL” may mean holiday pay. “PTO” means paid time off. “COMM” may mean commission, and “BONUS” is usually exactly what it sounds likethe fun line item everyone likes to see.

If your pay stub includes confusing codes, check your payroll portal, employee handbook, or ask HR or payroll. The important thing is not to guess. A mysterious deduction or earning code should not remain mysterious forever. Your paycheck is not a treasure map.

Way 2: Review Taxes, Deductions, and Net Pay

The second way to read a pay check stub is to move from what you earned to what was taken out. This is the part of the stub that explains why your gross pay and bank deposit are not identical twins.

Federal Income Tax Withholding

Federal income tax withholding is the amount your employer withholds from your paycheck and sends to the IRS on your behalf. The amount depends on your taxable wages, pay frequency, Form W-4 information, filing status, dependents, additional withholding, and other factors.

Your Form W-4 tells your employer how to calculate federal withholding. If too little is withheld, you may owe taxes when you file your return. If too much is withheld, you may receive a refund, but you also gave the government a no-interest loan. That is not always terrible, but it is worth understanding.

If your paycheck suddenly changes and you did not receive a raise, bonus, or deduction change, your withholding may be one reason. Major life eventsmarriage, divorce, a new child, a second job, a large raise, or buying a homecan make it smart to review your W-4.

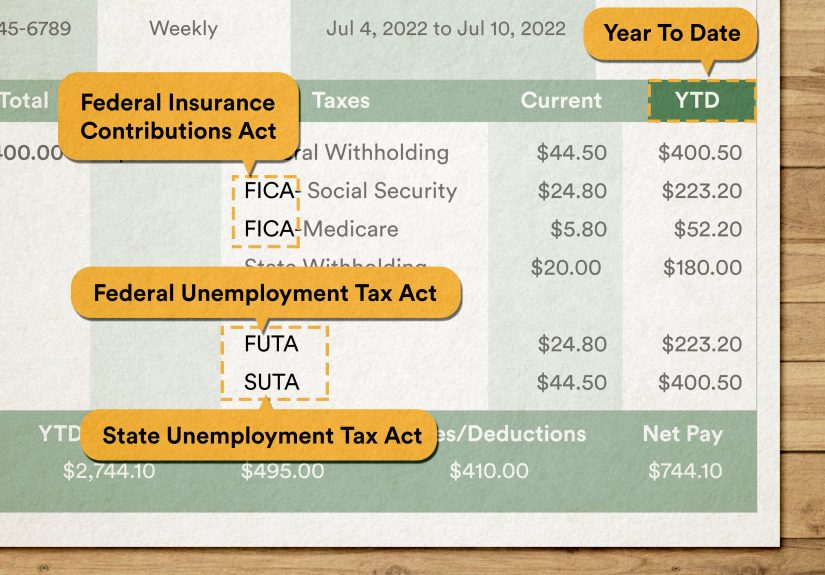

Social Security and Medicare Taxes

Most employees also see Social Security and Medicare taxes on their pay stubs. Together, these are commonly called FICA taxes. Social Security tax is withheld from employee wages up to an annual wage base limit. Medicare tax is generally withheld on all covered wages, with no wage base limit. High earners may also see Additional Medicare Tax once wages exceed the applicable threshold.

On a pay stub, Social Security may appear as “SS,” “OASDI,” or “FICA SS.” Medicare may appear as “MED,” “FICA MED,” or “Medicare.” These deductions fund Social Security and Medicare programs, not your employer’s secret office snack drawer.

If you are comparing paycheck math, remember that some pre-tax deductions may reduce wages subject to federal income tax, but not always in the same way for Social Security and Medicare. This is one reason your taxable wages may not match your gross wages exactly.

State and Local Taxes

Depending on where you live and work, your pay stub may show state income tax, local income tax, city tax, school district tax, state disability insurance, paid family leave contributions, unemployment-related deductions, or other state-specific items.

State and local payroll deductions vary widely. Someone working in Florida may not see state income tax withholding, while someone working in California, New York, Maryland, or another state with income tax rules may see several lines. Remote workers should pay special attention because the state where you live and the state where you work can affect withholding.

Voluntary Benefit Deductions

After taxes, your pay stub may list voluntary deductions. These are deductions you usually elected through your employer’s benefits program. Common examples include health insurance, dental insurance, vision insurance, life insurance, disability insurance, health savings account contributions, flexible spending account contributions, commuter benefits, union dues, charitable contributions, and retirement plan contributions.

Some deductions are pre-tax, meaning they reduce certain taxable wages before taxes are calculated. Others are post-tax, meaning they are taken after taxes. For example, traditional 401(k) contributions often reduce federal taxable income, while Roth 401(k) contributions are made after tax. Health insurance premiums under certain employer plans may be pre-tax. The label on the stub or benefits portal can help you tell the difference.

Garnishments and Required Deductions

Some deductions are not voluntary. Wage garnishments, child support orders, tax levies, or court-ordered payments may appear on a pay stub. If you see a required deduction you do not recognize, contact payroll immediately and request details. Do not ignore it and hope it becomes shy and leaves.

Net Pay: The Number That Actually Hits Your Account

Net pay is your take-home pay after all taxes and deductions are subtracted from gross pay. The basic formula is simple:

Gross Pay − Taxes − Deductions = Net Pay

For example, if your gross pay is $2,187.50 and your total deductions are $642.50, your net pay is:

$2,187.50 − $642.50 = $1,545.00 net pay

This is the amount you can use for budgeting, rent, groceries, savings, debt payments, and the occasional “I survived Monday” coffee.

Way 3: Check Year-to-Date Totals and Spot Red Flags

The third way to read a pay check stub is to review the year-to-date section, often labeled “YTD.” This part is easy to skip, but it is one of the most useful areas on the entire stub.

What YTD Means on a Pay Stub

Year-to-date totals show the cumulative amount earned, withheld, or deducted from the beginning of the calendar year through the current paycheck. Your stub may show YTD gross pay, YTD federal tax, YTD Social Security, YTD Medicare, YTD state tax, YTD retirement contributions, YTD insurance deductions, and YTD net pay.

Think of the current pay period as one episode and YTD as the full season recap. It helps you see the bigger picture.

Why YTD Totals Matter

YTD totals help you estimate annual income, track tax withholding, confirm retirement savings progress, and compare your final pay stub of the year with your Form W-2. Your W-2 will not always match every pay stub line perfectly because taxable wage categories differ, but your year-end pay stub can help you catch obvious issues before tax season.

YTD totals are also useful when applying for a mortgage, apartment lease, auto loan, student aid, or other financial product that requires proof of income. Some employers also report income and employment data to verification services, but your own pay stubs remain valuable records to keep.

Red Flags to Look For

When reading your pay stub, look for anything that seems off. Red flags may include missing overtime, incorrect hourly rates, pay period dates that do not match the work performed, deductions you did not authorize, benefits you canceled but are still paying for, retirement contributions that do not match your election, unusually high or low tax withholding, incorrect name or address, missing paid time off balances, or net pay that does not match your direct deposit.

Also check employer information. If you work for a company with multiple locations, divisions, or payroll entities, the employer name and address can matter for tax records and employment verification.

If something looks wrong, save a copy of the stub, write down your question, and contact payroll or HR. Be specific. Instead of saying, “My paycheck looks weird,” say, “My pay stub shows 80 regular hours, but my approved timecard shows 86 hours, including 6 overtime hours for the week ending March 14.” Specific questions get faster answers and make you sound like someone who brought receiptsbecause you did.

Sample Pay Stub Walkthrough

Let’s walk through a simple example. Imagine an employee named Jordan is paid every two weeks and earns $25 per hour. Jordan worked 80 regular hours and 5 overtime hours.

Regular pay: 80 hours × $25 = $2,000

Overtime pay: 5 hours × $37.50 = $187.50

Gross pay: $2,187.50

Jordan’s pay stub then shows the following deductions:

Federal income tax: $240

Social Security: $135.63

Medicare: $31.72

State income tax: $85

Health insurance: $90

401(k) contribution: $109.38

Total deductions equal $691.73. Jordan’s net pay is:

$2,187.50 − $691.73 = $1,495.77

By reading the stub in order, Jordan can confirm the hours, overtime rate, taxes, benefit deductions, retirement savings, and final take-home pay. That is the whole purpose of a pay stub: to make the paycheck explain itself.

Common Pay Stub Abbreviations

Pay stubs love abbreviations. Here are some common ones you may see:

Gross: Total earnings before deductions.

Net: Take-home pay after deductions.

YTD: Year-to-date totals.

FICA: Social Security and Medicare payroll taxes.

OASDI: Social Security tax.

MED: Medicare tax.

FIT or FITW: Federal income tax withholding.

SIT or SITW: State income tax withholding.

401(k): Employer-sponsored retirement plan contribution.

HSA: Health savings account contribution.

FSA: Flexible spending account contribution.

PTO: Paid time off.

Abbreviations vary by payroll provider, so do not panic if your stub uses slightly different labels. The core idea remains the same: earnings come in, deductions go out, net pay comes home.

How Often Should You Review Your Pay Stub?

Ideally, review every pay stub when it becomes available. You do not have to perform a full forensic audit each payday, but you should check the basics: pay period, hours, rate, gross pay, deductions, and net pay. A two-minute review can catch problems early.

Do a deeper review when you start a new job, change benefits, update your W-4, receive a raise, work overtime, earn a bonus, move states, change your retirement contribution, or notice a direct deposit amount that seems unusual. Paycheck mistakes are easier to fix when they are fresh.

Why Reading Your Pay Stub Helps Your Budget

Many people budget from salary, but bills are paid from net pay. That difference matters. A $60,000 salary does not mean $5,000 appears in your checking account every month. Taxes, insurance, retirement savings, and other deductions reduce your actual cash flow.

When you understand your pay stub, you can build a realistic budget. You can also decide whether to increase retirement contributions, adjust tax withholding, change benefits during open enrollment, or set up automatic savings. Your pay stub is not just a payroll document; it is a financial planning tool wearing a very boring outfit.

Experience-Based Tips for Reading a Pay Check Stub

One of the best habits you can build is saving every pay stub, even if your employer keeps digital copies. Payroll portals can change, accounts can close after you leave a job, and old records can become harder to access right when you need them. Downloading a PDF each payday may feel unnecessary, but future you may send present you a thank-you note.

A practical experience many workers share is that the first paycheck at a new job often looks smaller than expected. This does not always mean something is wrong. The first check may cover a partial pay period, include benefit deductions, reflect new tax withholding, or exclude a bonus that starts later. Still, review it carefully. Confirm your hourly rate or salary, pay period dates, and deductions. If your first pay stub is wrong, fixing it early prevents the same error from repeating.

Another useful tip is to compare your pay stub to your benefits elections after open enrollment. For example, if you selected a lower-cost health plan but your deduction still reflects the old plan, payroll may need to correct it. If you increased your 401(k) contribution from 4% to 6%, check whether the new percentage appears on the next paycheck. Small benefit mistakes can quietly drain hundreds of dollars over the year.

Hourly employees should pay extra attention to overtime, shift differentials, and paid time off. These items are more likely to vary from one paycheck to the next. If you work nights, weekends, holidays, or split shifts, your stub may have multiple earning lines. Read each one. A missing differential may look small on one check, but repeated over months, it becomes real money.

Salaried employees should not ignore pay stubs just because the gross amount looks the same each period. Deductions can change. Tax withholding can change. Retirement contributions can change. Insurance premiums can change. A steady salary does not guarantee a steady net paycheck.

It also helps to create a simple paycheck checklist. Before you move on with your day, ask: Are the pay period dates correct? Is my gross pay reasonable? Are my hours right? Did overtime appear? Are my deductions familiar? Does net pay match my deposit? Are YTD totals moving in the right direction? That checklist turns a confusing document into a quick routine.

If you find an error, stay calm and document everything. Payroll teams handle lots of moving parts, and many mistakes are fixable. Send a clear message with the pay date, pay period, specific line item, and what you expected to see. Attach supporting records such as a timecard, offer letter, benefits confirmation, or written approval for overtime. The clearer your message, the faster the issue can usually be resolved.

Finally, use your pay stub as a reality check for financial goals. If you want to save more, your stub shows where money is already going. If you want a smaller tax refund and larger paychecks, your withholding section gives you a place to start. If you want to increase retirement savings, your contribution line shows your current progress. Reading your pay check stub is not just about catching mistakes; it is about understanding your money before it disappears into bills, subscriptions, and suspiciously expensive takeout.

Conclusion

Learning how to read a pay check stub gives you more control over your money. Start with your earnings and gross pay, then review taxes and deductions, and finally check your year-to-date totals for the bigger picture. These three steps help you understand where your money comes from, where it goes, and whether your paycheck is accurate.

Your pay stub may never become thrilling bedtime reading, but it is one of the most important financial documents you receive. It can help you catch payroll errors, prepare for taxes, verify income, track benefits, monitor retirement savings, and build a budget based on actual take-home pay. In short, your pay stub is not just paperwork. It is your paycheck’s instruction manualand yes, this is one instruction manual worth reading.