Table of Contents >> Show >> Hide

- What a Credit Card Actually Does

- Why Almost Everyone Benefits From Having One

- 1. It Helps You Build a Credit History

- 2. It Offers Stronger Fraud and Dispute Protection

- 3. It Makes Travel, Hotels, and Rental Cars Less Annoying

- 4. It Can Improve Cash Flow Without Costing Interest

- 5. Rewards Are Nice, Even If They Should Not Be the Main Reason

- 6. It Helps You Build Financial Independence

- Why the Word “Almost” Matters

- How to Use a Credit Card Without Paying Interest

- What Kind of Card Makes Sense for Most People?

- Common Credit Card Mistakes to Avoid

- Real-World Experiences: What Having a Credit Card Looks Like in Practice

- Final Thoughts

Let’s start with a sentence that would make some personal finance gurus clutch their spreadsheets: for most adults, having a credit card is a smart move. Not because swiping plastic is glamorous. Not because rewards points will transform you into a free-flight wizard. And definitely not because debt is fun. It is not. Debt is basically the party guest who eats all your snacks and never leaves.

But a well-used credit card can help you build credit, protect your money, make travel and online shopping easier, and create a financial cushion between “I bought groceries today” and “my checking account updates tomorrow.” In modern American life, a credit card is often less of a luxury and more of a practical tool. The trick is simple to say and harder to do: use it like a debit card with better benefits, not like free money from the universe.

That is where the “almost” comes in. Nearly everyone can benefit from a credit card, but not everyone should open one this afternoon. If you are deep in debt, dealing with compulsive spending, or struggling to cover essentials, a credit card can make a tough situation worse. For everyone else, though, the right card plus the right habits can do a lot of heavy lifting for your financial life.

What a Credit Card Actually Does

A credit card gives you access to a revolving line of credit. You make purchases now, receive a statement later, and then choose how much to pay by the due date. If you pay the statement balance in full every month, you can usually avoid interest on purchases. If you carry a balance, interest starts doing what interest does best: quietly multiplying while pretending to be helpful.

This is why a credit card is not automatically dangerous. The danger comes from how it is used. A hammer can build a bookshelf or smash your thumb. A credit card can build credit and add protections, or it can become a very efficient debt machine. Same tool, wildly different outcome.

Why Almost Everyone Benefits From Having One

1. It Helps You Build a Credit History

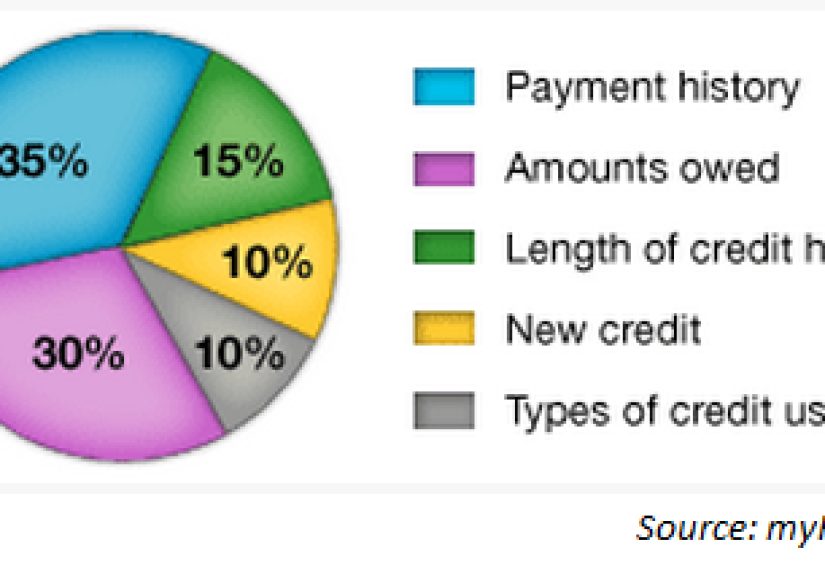

The biggest reason most people need a credit card is boring, powerful, and very real: credit history matters. Your credit profile can affect whether you qualify for an apartment, a car loan, a mortgage, or better borrowing terms. In some situations, it can even affect utility deposits or insurance pricing.

A credit card is one of the easiest ways to start building that history. Use it regularly, keep the balance low relative to the limit, and pay on time every month. That creates the kind of record lenders like to see. You do not need five premium cards and an app that sends you confetti every time you buy coffee. One starter card used responsibly is often enough to begin building a strong foundation.

Think of it this way: if you never use credit, lenders have less evidence that you can handle it. That is frustrating, but it is how the system works. A credit card gives you a relatively simple, controlled way to show that you can borrow money, manage it, and pay it back without drama.

2. It Offers Stronger Fraud and Dispute Protection

Credit cards usually provide better practical protection than cash and often create less immediate pain than debit cards when something goes wrong. If your debit card is compromised, the problem can hit your bank account directly. Rent money, grocery money, and bill money may all suddenly be starring in a thriller you did not buy tickets for.

With a credit card, unauthorized charges are generally easier to separate from your actual cash. You can dispute billing errors, flag suspicious activity, and avoid having your checking balance tied up while the issue is investigated. That matters in real life. Fraud is not just a technical inconvenience; it is a timing problem. When money disappears at the wrong moment, even temporarily, everything else gets harder.

This is one reason many financially careful people put online purchases, travel bookings, and other high-risk transactions on a credit card instead of a debit card. It creates a buffer between the merchant ecosystem and the money you use to live on.

3. It Makes Travel, Hotels, and Rental Cars Less Annoying

There are few modern experiences more humbling than arriving at a hotel desk after a long trip and discovering there is an authorization hold bigger than expected. Hotels, gas stations, and rental car companies often place temporary holds. A credit card handles those holds more gracefully because they reduce available credit rather than freezing your bank balance.

That can be the difference between “slightly annoying” and “why is my checking account gasping for air?” Even beyond holds, credit cards can make travel easier through better acceptance, simpler booking, potential travel protections, and clearer expense tracking.

No, a credit card will not fix delayed flights or magically improve airport food. But it can make the financial side of travel smoother, which is the closest thing to peace many travelers will get before boarding Group 9.

4. It Can Improve Cash Flow Without Costing Interest

Used correctly, a credit card can give you short-term breathing room between purchase date and payment date. That does not mean spending beyond your means. It means matching your routine expenses to a billing cycle, keeping your cash in your account until the bill is due, and paying the full statement balance on time.

For organized users, this creates a cleaner monthly system. Instead of random transactions splashing around your checking account every day, many purchases collect into one statement. That makes budgeting easier to review and easier to correct. You can quickly see whether your money went to groceries, takeout, subscriptions, or your recurring habit of buying things online at 11:42 p.m. because they were “on sale.”

5. Rewards Are Nice, Even If They Should Not Be the Main Reason

Cash back, points, miles, statement credits, extended warranties, purchase protections, and travel perks can all add value. But let’s keep the confetti cannon off for a second: rewards only matter if you are not paying interest. Earning 2% cash back while carrying a balance at a high APR is like finding a coupon while your roof is on fire.

Still, for people who pay in full every month, rewards can be genuinely useful. A flat-rate cash-back card is often the easiest win. It is simple, flexible, and does not require a PhD in airline alliances. For frequent travelers, a card with no foreign transaction fees or useful trip protections can also make sense.

6. It Helps You Build Financial Independence

For young adults especially, a first credit card can be more than a payment tool. It can be a training ground. Learning how due dates work, how utilization affects your profile, how statements differ from current balances, and how autopay saves your future self from dumb mistakes is part of adult financial fluency.

Used responsibly, a credit card teaches money management in a way theory never quite can. Reading about healthy habits is nice. Setting a small recurring bill on a card, paying it off every month, and watching your credit strengthen is better.

Why the Word “Almost” Matters

Now for the part that deserves flashing lights: a credit card is not the right move for everyone at every moment.

Who may want to wait

If you routinely spend more than you earn, miss bill due dates, or already feel overwhelmed by debt, opening a new card may add fuel instead of help. The same goes for people who know they are prone to impulse spending. Self-awareness is not defeat. It is strategy.

In those cases, it may be smarter to pause, stabilize your budget, build a small emergency fund, or start with a secured card that has a low limit and a very specific purpose. A credit card should support your system, not replace one.

Who should be extra careful

Students, first-time users, and anyone recovering from credit mistakes should keep things simple. One card. One or two recurring expenses. Autopay enabled. Regular account review. No “I’ll totally pay this off later” speeches. Those speeches have a terrible success rate.

How to Use a Credit Card Without Paying Interest

This is the part that turns a card from useful tool into financial sidekick:

Pay the statement balance in full

Not the minimum. Not “most of it.” The full statement balance by the due date. That is the habit that protects you from interest on standard purchases.

Keep utilization low

Even if you can spend more, do not treat your limit like a suggestion from destiny. Lower balances relative to your limit are generally better for your credit profile.

Automate at least the minimum payment

Autopay is not cheating. It is adult wisdom. Even if you prefer to pay manually, setting automatic minimum payments can protect you from accidental late fees and credit damage.

Use alerts

Set alerts for due dates, large purchases, and unusual activity. Your future self will appreciate not discovering a problem three weeks late while waiting in line for tacos.

Do not chase rewards by overspending

The best rewards strategy is boring: spend what you were already going to spend, then collect the benefits. Buying unnecessary stuff for points is how “free rewards” quietly become very expensive decor.

What Kind of Card Makes Sense for Most People?

For beginners, the best first card is usually not the flashiest. It is the one you can manage easily.

Good options include:

A no-annual-fee cash-back card: Great for simplicity and everyday spending.

A secured credit card: Useful if you are building or rebuilding credit.

A student card: Helpful for younger users who want to establish a history.

A travel card: Better for people who already travel often and understand the fee-and-benefit tradeoff.

In general, simple beats clever. A complicated rewards system is not a personality trait. If a plain card helps you build credit and stay organized, that is already a win.

Common Credit Card Mistakes to Avoid

Most credit card problems do not come from the card itself. They come from a few predictable habits:

Carrying a balance for routine spending. If you are using next month’s income to pay for last month’s takeout, something needs adjusting.

Missing due dates. Late payments can cost money and hurt your credit.

Maxing out the card. High utilization can stress your budget and your credit profile.

Opening cards for every sign-up bonus. This is advanced mode. Most people should not start there.

Ignoring statements. Billing errors and fraud are much easier to fix when caught early.

Real-World Experiences: What Having a Credit Card Looks Like in Practice

Experience number one is the classic first-card story. Someone opens a simple no-annual-fee card, puts one subscription and a monthly grocery run on it, turns on autopay, and barely thinks about it. Six months later, their credit profile is stronger, they understand statements better, and they no longer feel like credit scores are mystical numbers generated by forest wizards.

Experience number two is the online-shopping save. A cardholder notices a strange charge from a retailer they have never used. Instead of panicking about whether their checking account can still cover bills, they report the charge, freeze the card, and get a replacement. It is still annoying, but it is administrative annoying, not rent-is-now-a-mystery annoying. That distinction matters more than people realize.

Experience number three shows up during travel. A hotel places a temporary hold, then a rental car company does the same thing, and suddenly the traveler is glad those holds are hitting available credit instead of draining cash from a debit-linked account. Add in the convenience of one clear statement after the trip, and the credit card starts to feel less like a luxury perk and more like sensible equipment.

Experience number four is the “I thought minimum payments were fine” lesson, which is the personal finance equivalent of touching a hot stove after being told not to. At first, the minimum seems manageable. Then interest starts stacking up, balances stop shrinking, and the card that once felt helpful becomes expensive. A lot of adults learn this the hard way. The good news is that the lesson sticks: pay in full whenever possible, and never confuse “allowed” with “wise.”

Experience number five is about rebuilding. Someone who had past credit trouble starts over with a secured card and a tiny limit. No fancy perks. No airport lounge fantasies. Just steady, careful use. Over time, on-time payments and low balances begin doing their quiet work. This experience matters because it proves credit cards are not only for people with perfect finances. They can also be stepping stones for people trying to improve.

Experience number six is the budgeting surprise. Many users find that putting predictable expenses on one card actually makes them more disciplined, not less. A monthly statement creates a clean record. It becomes easier to notice patterns, like how much goes to food delivery, subscriptions, or random impulse buys disguised as “household needs.” Suddenly the card is not encouraging chaos; it is exposing it.

And then there is the mature-cardholder experience, which is delightfully unglamorous. They use the card for ordinary expenses, review statements, redeem cash back once in a while, and pay the balance in full every month. No drama. No revolving debt. No heroic optimization spreadsheets. Just a practical financial habit that quietly makes life easier. Honestly, that is the dream. Not luxury. Not status. Just useful, predictable competence.

Final Thoughts

So, why does almost everyone need a credit card? Because modern financial life rewards people who can build credit, protect their cash, handle digital purchases safely, and move through everyday transactions with less friction. A credit card can help with all of that.

But the best credit card strategy is not flashy. It is disciplined. Get a card that fits your life, keep your spending controlled, pay your statement balance in full, and let time do its thing. Used this way, a credit card is not a debt trap. It is a tool. A very useful one. Kind of like a fire extinguisher, but with cash back.