Table of Contents >> Show >> Hide

- What “SaaS” actually means (and why it matters)

- So where did the $116B “next year” number come from?

- Why SaaS growth keeps happening (even when budgets get grumpy)

- From $116B to “wait… it’s HOW much now?”

- The business engine under SaaS: why investors (and CFOs) obsess over these metrics

- What SaaS looks like for buyers: the good, the bad, and the “who approved this?”

- What’s pushing SaaS forward now: AI, verticalization, and the “workflow war”

- So… is $116B still “wow”?

- Experiences from the SaaS trenches (the last 500-ish words you’ll thank yourself for)

- Conclusion

“SaaS will hit $116 billion next year.” If you read that line and your first reaction was

“Wait… is that a typo?”welcome to cloud economics, where the numbers are large, the acronyms are

larger, and your finance team is quietly weeping into a spreadsheet named “Renewals_FINAL_v12_reallyfinal.xlsx.”

The $116B headline comes from a well-known forecast that pegged Software as a Service as the

biggest slice of public cloud spending at the time. And it was a “wow” number. But here’s the real twist:

the story didn’t stop at $116B. Not even close. In more recent forecasts, SaaS spending in the public cloud

ecosystem is measured in the hundreds of billions annually. So yes$116B is wow. It’s also the opening act.

What “SaaS” actually means (and why it matters)

SaaSSoftware as a Serviceis the model where you access software over the internet and pay

on a subscription or consumption basis instead of installing and maintaining it yourself. Think email suites,

CRMs, help desks, analytics tools, project management platforms, HR systems, and the 47 “quick experiments”

that became mission-critical in about a week.

SaaS vs. “cloud” vs. “public cloud spending” (yes, these differ)

One reason SaaS stats get confusing is that different reports measure different things:

- SaaS is a service model (software delivered over the cloud).

- Public cloud spending is a broader bucket that can include SaaS, infrastructure (IaaS), platforms (PaaS), and sometimes other cloud services depending on the taxonomy.

- Cloud infrastructure market stats often focus on IaaS/PaaS (the “pipes and engines”), not SaaS apps.

Translation: two numbers can both be true and still look wildly different because they’re counting different

parts of the cloud elephant.

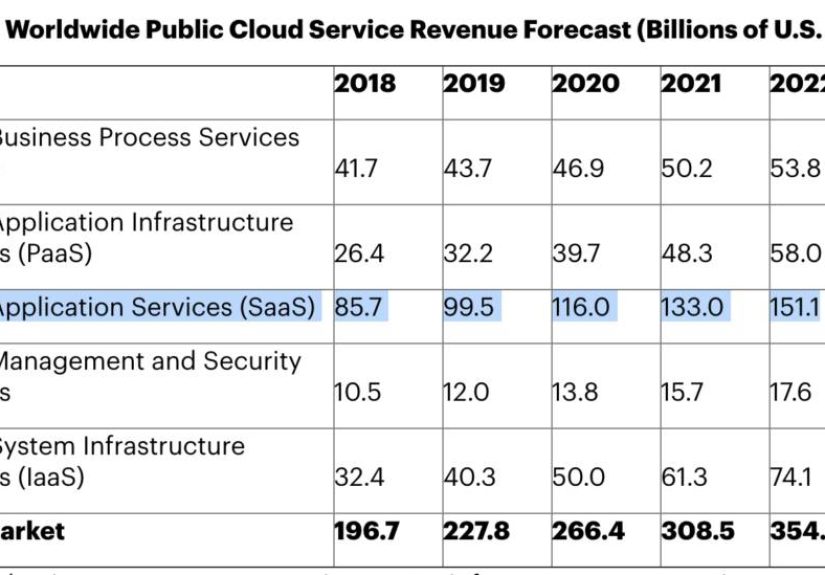

So where did the $116B “next year” number come from?

In late 2019, a major industry forecast projected that SaaS (then the largest segment of public cloud services)

would reach $116.0B in 2020. At the time, the same forecast showed SaaS at $99.5B in 2019,

with continued growth expected into subsequent years. In other words: SaaS wasn’t just bigit was becoming

the default delivery model for business software.

If you’re wondering why SaaS grew so quickly, a good starting point is that the subscription model scales

like a meme: once it’s easy to adopt, it spreads. And unlike the office fridge mystery container, SaaS

tends to deliver value immediatelyprovided you don’t turn onboarding into an endurance sport.

Why SaaS growth keeps happening (even when budgets get grumpy)

SaaS has a few structural advantages that don’t disappear when the economy gets moody:

1) Faster time-to-value

Traditional software often meant procurement, servers, configuration, upgrades, and a small pilgrimage to

the IT gods. SaaS compresses that timeline: you sign up, configure, integrate, and ship value to users.

The speed advantage is hard to give up once you’ve tasted it.

2) Elasticity (a fancy word for “it grows with you”)

Growing companies like SaaS because it scales up quickly. Shrinking companies like SaaS because it can

scale down faster than a data-center lease. In theory. In practice, you still need to track seats, plans,

and “that one department” that bought the enterprise tier for three people.

3) Continuous improvements

SaaS vendors push frequent updatesnew features, security patches, performance improvementswithout customers

coordinating big upgrade projects. This shift from “annual upgrade drama” to “quiet weekly improvements”

changes how organizations modernize.

4) The integration flywheel

SaaS is rarely a single app. It’s an ecosystem: APIs, connectors, workflow automation, identity providers,

data warehouses, and now AI assistants that promise to “just handle it.” The more connected the ecosystem,

the more switching costs riseand the more SaaS becomes embedded.

From $116B to “wait… it’s HOW much now?”

Here’s where the narrative gets fun. More recent public cloud spending forecasts put SaaS at roughly

$247B–$251B in 2024 and around $295B–$299B in 2025, depending on the specific forecast update and segment definitions.

That’s not a gentle climb. That’s a rocket with a subscription billing engine.

Meanwhile, overall public cloud spending has been projected in the hundreds of billions annually,

with growth driven by modernization and AI-enabled workloads. In plain English: SaaS isn’t just a software

category anymoreit’s a delivery assumption for a massive share of business applications.

Why forecasts sometimes “move”

If you see slightly different totals across reputable forecasts, it’s often because the segmentation changes.

Some models include additional cloud categories (like business process services), while others focus on a narrower set

(SaaS, PaaS, IaaS, desktop-as-a-service). The key point is directional: SaaS remains enormousand growing.

The business engine under SaaS: why investors (and CFOs) obsess over these metrics

SaaS is not just “software on the internet.” It’s a business model with distinctive economics. That’s why

SaaS companies talk in a dialect that sounds like finance and product had a baby:

ARR (Annual Recurring Revenue), MRR (Monthly Recurring Revenue),

NRR (Net Revenue Retention), CAC (Customer Acquisition Cost), and

LTV (Lifetime Value).

Retention is the cheat code (and everyone’s trying to re-find it)

In SaaS, growth isn’t just about new customers. It’s also about how much existing customers expandor shrink.

Over the last few years, many benchmark reports noted softer retention dynamics compared to earlier boom years,

which pushed SaaS operators to focus on adoption, expansion revenue, and pricing discipline.

Practical examples of retention work that actually moves the needle:

- Shorten time-to-first-value: If the first week feels like filing taxes, churn is coming.

- Make outcomes visible: Dashboards that show measurable wins reduce “why are we paying for this?” moments.

- Usage-based nudges: Product cues that guide users to the next value milestone (without being annoying).

- Right-size plans: Tiering should feel like a ladder, not a trapdoor.

CAC payback and “efficient growth” (because money isn’t free anymore)

When capital is cheap, companies can prioritize speed. When capital is not cheap, efficiency becomes a love language.

That’s why SaaS leaders focus on CAC payback (how fast you recover what you spent to acquire a customer)

and operating discipline. Recent industry surveys and benchmark discussions have emphasized operational excellence,

AI-driven product shifts, and more measured go-to-market spending.

The Rule of 40 (a simple benchmark with a surprisingly long shadow)

The Rule of 40 is a popular heuristic: a healthy SaaS company often targets

growth rate + profit margin ≈ 40. It’s not a law of physics, but it’s a useful sanity check.

In the real world, the “right” balance depends on stage, market size, and competitive dynamics.

Still, the Rule of 40 remains a north star because it forces a tradeoff conversation:

Are we growing fast enough to justify our spend? Or profitable enough to justify our pace?

What SaaS looks like for buyers: the good, the bad, and the “who approved this?”

If you buy SaaS for a living (or accidentally became the person who does), the experience is a mix of joy and chaos:

- Joy: faster deployments, lower ops burden, frequent improvements, easier collaboration.

- Chaos: overlapping tools, hidden renewals, access sprawl, and “Shadow IT” that appears overnight.

How to avoid SaaS sprawl without becoming the “No” department

The goal isn’t to stop teams from adopting tools. It’s to make adoption visible, secure, and financially sane.

A practical governance approach often looks like this:

- Inventory first: You can’t manage what you can’t seeapps, owners, spend, renewal dates, and usage.

- Standardize procurement: A lightweight intake process beats 90 surprise renewals.

- Centralize identity: SSO, MFA, and automated provisioning reduce risk and offboarding pain.

- Measure adoption: If a tool is paid for but unused, it’s not a “platform,” it’s a donation.

- Plan exits: Data export, contract terms, and migration paths should exist before you need them.

Security in SaaS: “shared responsibility” isn’t a sloganit’s the job description

A common misunderstanding is: “It’s SaaS, so the vendor handles security.” The reality is more nuanced.

Cloud security follows a shared responsibility modelthe provider secures the underlying systems,

but customers still own key responsibilities such as identity, access controls, configuration, and data governance.

What that means in plain terms:

- Vendors typically handle the application infrastructure, patching, and baseline platform security.

- You still handle user access, roles, MFA, data sharing settings, and how sensitive data is stored and exported.

The punchline: SaaS can reduce security burden, but it does not outsource accountability. If your admin account gets phished,

the attacker won’t politely stop because your vendor has a strong SOC team.

What’s pushing SaaS forward now: AI, verticalization, and the “workflow war”

SaaS is evolving from “apps with logins” to “systems that run work.” Three trends show up again and again:

AI features are becoming table stakes

Many SaaS products are embedding AI to summarize, generate, classify, recommend, and automate. The competitive shift

is moving from “who has AI?” to “who has AI that reliably improves outcomes?” Expect more focus on governance,

auditability, and data controlsbecause nobody wants an assistant that confidently invents policies.

Vertical SaaS keeps winning in messy industries

Horizontal tools are powerful, but vertical SaaS (built for specific industries like healthcare, construction,

logistics, or financial services) often wins by speaking the industry’s native language: workflows, compliance,

reporting, and edge cases that general tools treat like “nice-to-haves.”

Platforms are consolidating, while best-of-breed still survives

Buyers want fewer vendors and simpler integration. But teams also want specialized tools that do one job extremely well.

The likely outcome is a “platform core + specialist edges” model: a central suite for identity, data, and collaboration,

surrounded by niche apps that integrate cleanly and prove their ROI fast.

So… is $116B still “wow”?

Yesand also no. It’s “wow” because $116B represented a milestone: SaaS becoming the largest public cloud segment

and a default delivery model for modern software. It’s “no” because today’s forecasts place SaaS spending far beyond

that figure. The bigger takeaway isn’t the exact number; it’s the direction of travel:

software keeps moving toward services, and organizations keep funding that shift because it delivers speed, flexibility, and continuous valuewhen managed well.

If you’re building SaaS: the bar is rising. Users expect instant value, secure-by-default systems, and pricing that feels fair.

If you’re buying SaaS: the opportunity is enormous, but so is the need for governance, security hygiene, and ruthless clarity about outcomes.

Experiences from the SaaS trenches (the last 500-ish words you’ll thank yourself for)

Let’s talk about the part nobody puts in glossy market forecasts: what it actually feels like to live in a SaaS world.

Because whether you’re a founder, a product leader, an IT admin, or the unlucky soul tasked with “vendor management,” the day-to-day

reality is a mix of empowerment and entropy.

One common experience: the SaaS stack grows faster than your org chart. A team adopts a tool for a “pilot.”

Another team adopts a competing tool because the first tool “didn’t have the feature” (which it did, but the feature was buried under

three menus and a settings toggle named after a Greek philosopher). Suddenly, you’re paying for two subscriptions, both underused, and

nobody remembers who owns the renewal. The cost isn’t just moneyit’s cognitive load.

Another experience: onboarding is the silent killer. SaaS companies love to say, “Easy to get started!”

And yessigning up is easy. Getting the organization to actually change behavior is the hard part.

Real adoption usually needs clear use cases, training that respects people’s time, a champion inside the team, and integration with

the tools users already live in. When onboarding is done well, SaaS feels like magic. When it’s done poorly, SaaS feels like

you bought a treadmill that mostly holds laundry.

Then there’s the classic: security settings that are optional… until they aren’t. Many teams discoverlatethat

“SaaS security” is not a single toggle. It’s MFA enforcement, role hygiene, audit logs, data sharing controls, API keys, third-party

integrations, and access reviews. The shared responsibility model becomes painfully real the first time someone shares a sensitive file

publicly, invites a personal email into a corporate workspace, or leaves an admin account with a password that can be guessed by a determined

golden retriever.

For builders, a frequent experience is pricing and packaging whiplash. Customers want simple pricing, but their needs

aren’t simple. Founders experiment with per-seat, per-usage, tiered plans, add-ons, and enterprise contracts that look like they were negotiated

by medieval guilds. Meanwhile, the product keeps evolvingespecially with AI features that have real compute costs. The best SaaS businesses

learn to align pricing with value: not “how many buttons you can click,” but “how much outcome you can reliably achieve.”

And finally, the most human experience: renewal season. Renewal season is when everyone suddenly becomes philosophical.

“Do we still need this?” “Are we using it?” “Could we replace it?” “Who owns it?” “Why are we paying for 300 seats when we have 120 employees?”

The organizations that handle renewal season well tend to do the boring work all year: usage tracking, clear ownership, periodic access reviews,

and a simple policy that says, “If it’s paid for, it must be measurable.” Boring? Yes. Effective? Absolutely.

If SaaS is headed toward ever-larger numbersand it isthe winners won’t just be the companies with the biggest market.

They’ll be the ones who make adoption easy, outcomes obvious, governance painless, and security unavoidable (in the best way).

Because in the end, SaaS isn’t about software. It’s about work. And work always finds the tools that get out of the way.

Conclusion

“SaaS will hit $116B next year” was a headline that captured a turning point: subscriptions and cloud delivery were no longer a trendthey were

the default. Since then, the market has continued to expand, shaped by modernization, integration ecosystems, security realities, and now AI-driven workflows.

Whether you’re building, buying, or managing SaaS, the opportunity is massivebut so is the need for clarity: know what you’re paying for,

prove the outcome, and treat governance as a growth strategy (not a buzzkill).