Table of Contents >> Show >> Hide

- Why This Debate Matters Right Now

- Point: The Case for Real Estate as an Investment Option

- Counterpoint: The Case Against Real Estate as an Investment Option

- The Middle Ground: Real Estate Is Not One Thing

- Who Real Estate May Be Best For

- Who May Want to Be Cautious (or Choose Another Route)

- A Practical Decision Framework Before You Invest

- Extended Experience Section (About ): What Investors Commonly Learn the Hard Way

- Conclusion: The Real Point/Counterpoint Answer

Real estate is the investment world’s version of a pickup truck: practical, popular, and occasionally expensive to repair at the worst possible time. Some investors swear by it as the ultimate wealth-building machine. Others see it as a capital-hungry, stress-generating side job with surprise plumbing bills. The truth? Both camps have a point.

If you are deciding whether real estate deserves a place in your portfolio, the best approach is not hype or doomposting. It is a clean point/counterpoint analysis: What does real estate do really well, where does it fall short, and for what type of investor does it actually make sense? This guide breaks that down in plain English, with practical examples, risk analysis, and a few reality checks for anyone tempted by “passive income” videos filmed in suspiciously perfect kitchens.

Why This Debate Matters Right Now

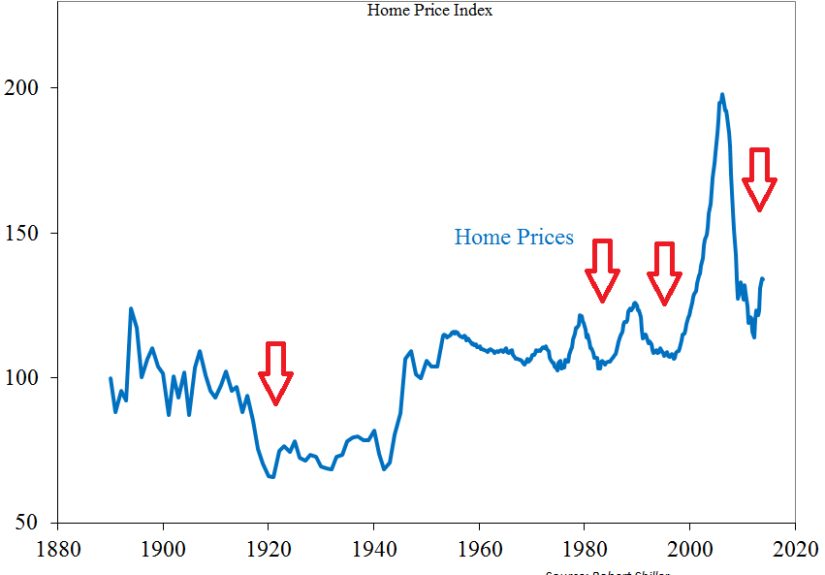

Real estate has always been a major wealth-building path in the U.S., but today’s environment makes the decision more nuanced. Higher borrowing costs can squeeze cash flow. Insurance and maintenance expenses can jump. At the same time, limited housing supply in many markets and long-term demand for rentals can still support strong investment cases. In other words: real estate is neither automatically brilliant nor automatically bad. It is highly sensitive to purchase price, financing, location, and execution.

That is why “Should I invest in real estate?” is the wrong first question. A better one is: Which type of real estate investment, at what price, with what risks, and compared to what alternative? Once you ask that, the conversation gets smarter fast.

Point: The Case for Real Estate as an Investment Option

1) It Can Produce Income While You Hold It

The biggest argument in favor of real estate is simple: a properly bought and managed property can generate recurring cash flow. Rent comes in monthly, while your mortgage payment (if fixed) stays predictable. Over time, rents may rise, potentially improving income margins if expenses are under control.

For investors who like tangible income-producing assets, this is appealing. Unlike a growth stock that might (or might not) pay dividends later, a rental property can start producing revenue right away. That said, “revenue” is not the same as “profit,” and we will get to that in the counterpoint section before anyone buys a fourplex using pure optimism.

2) Leverage Can Magnify Returns

Real estate is one of the few mainstream investments where ordinary investors commonly use large amounts of financing. With a down payment, you control an asset worth much more than the cash you put in. If the property appreciates and cash flows well, leverage can meaningfully boost your return on invested capital.

This is one reason real estate investors often build wealth faster than expected when they buy conservatively and hold for years. Mortgage amortization can also work in your favor: tenants may effectively help pay down the loan principal while you retain ownership of the asset.

3) It Is a Tangible Asset You Can Improve

Stocks usually do not let you repaint management, but real estate lets you create value directly. You can renovate a kitchen, add a bathroom, improve curb appeal, reduce operating costs, or convert an underperforming layout into a more rentable space. That level of control is a major advantage for hands-on investors.

In practical terms, real estate returns often come from operations and execution, not just market appreciation. A mediocre property can become a strong performer with good management, better tenant screening, and smarter capital improvements.

4) Tax Benefits Can Be Meaningful

Tax treatment is another reason real estate remains attractive. Rental property owners may be able to deduct certain operating expenses and depreciate the building over time, which can reduce taxable income. However, the tax side is not “free money”; it is a rules-heavy area with important distinctions between repairs and improvements, rental use and personal use, and current deductions versus capitalized costs.

Translation: tax benefits are real, but so is tax complexity. A good CPA can be worth more than a “hot market” tip from a stranger on social media.

5) Diversification and Behavioral Benefits

For some investors, real estate adds diversification because it behaves differently from stocks and bonds. It can also be psychologically easier to hold through volatility. A rental property does not flash a red number at you every second like a brokerage app. For certain personalities, that reduces panic-selling and helps them stay invested longer.

Real estate can also align with life goals. House hacking, buying a duplex, or owning a rental near family may offer both financial and practical benefits that traditional investments do not.

Counterpoint: The Case Against Real Estate as an Investment Option

1) It Is Illiquid and Expensive to Buy/Sell

Real estate is not a tap-to-sell asset. Transactions can take weeks or months, and the costs around buying and selling are substantial. Beyond the purchase price, investors face appraisal fees, title-related costs, insurance prepaids, taxes, and other closing expenses. Selling later can add agent commissions and more transactional friction.

This matters because liquidity is not just convenience; it is risk management. If you need cash fast, a property is a stubborn asset. Real estate may be great for long-term wealth building, but it is not ideal for emergency liquidity.

2) Cash Flow Is Easy to Overestimate

New investors often run numbers like this: “Rent is $2,500 and the mortgage is $2,000, so I make $500 a month.” That math is adorable. It is also incomplete.

Real cash flow must account for property taxes, insurance, maintenance, repairs, capital expenditures (roof, HVAC, appliances), vacancy, leasing costs, utilities (if paid by owner), HOA dues, property management fees, and legal/accounting costs. One expensive repair can erase months of profits.

Real estate can absolutely cash flow, but only if you underwrite conservatively and assume bad months will happen. Because they will.

3) Leverage Amplifies Losses Too

The same leverage that boosts returns can magnify pain. If rents decline, occupancy drops, or financing costs are high, a leveraged property can turn into a monthly cash drain. Investors who buy with thin margins may discover that “positive cash flow” disappears the moment insurance renews or the water heater gives up on life.

Debt also introduces timing risk. Even if a property is a good long-term asset, refinancing or selling during a weak market can materially hurt returns.

4) It Is Not Truly Passive for Most People

Direct real estate ownership is often described as passive income, but for many investors it is more like “income with a to-do list.” Tenant screening, maintenance calls, turnover coordination, bookkeeping, vendor management, lease renewals, compliance, and dispute handling all take time.

Hiring a property manager helps, but that reduces net income and does not remove owner responsibility. You still need to review statements, approve repairs, and monitor performance. If you want a truly passive real-estate-like exposure, a REIT or real estate fund may fit better than owning a rental house directly.

5) Regulation and Compliance Risk Are Real

Housing is heavily regulated, and investors must comply with fair housing laws and applicable state/local landlord-tenant rules. Screening policies, advertising language, lease enforcement, security deposit handling, and eviction procedures can all create legal exposure if managed poorly.

This does not mean landlords are doomed. It means real estate is a business, and businesses require compliance systems. If you dislike paperwork, documentation, and rule-following, direct ownership may feel like wearing a suit made of receipts.

6) Insurance, Climate, and Property-Specific Risks Can Change the Math

A property may look excellent on paper until insurance quotes arrive. In some areas, rising insurance costs, deductibles, or coverage limitations can significantly impact net returns. Flood risk is especially important because standard homeowners insurance typically does not cover flood damage, and separate flood coverage may be needed.

The key takeaway: location analysis is no longer just neighborhood, school district, and rent comps. It also includes insurability, disaster exposure, and resilience-related costs.

The Middle Ground: Real Estate Is Not One Thing

Many debates about real estate go off the rails because people compare totally different strategies. A single-family rental in a high-cost coastal market is not the same as a small multifamily in the Midwest. A private non-traded REIT is not the same as a publicly traded REIT ETF. A short-term rental is not the same as a long-term lease.

Direct Ownership vs. REITs

If you want control, potential tax advantages, and the ability to force appreciation, direct ownership may be attractive. If you want liquidity, easier diversification, and less operational hassle, publicly traded REITs can offer a simpler way to get real estate exposure.

However, not all REITs are equal. Publicly traded REITs are generally easier to price and sell. Non-traded REITs can involve liquidity constraints, valuation opacity, and higher upfront fees. That does not make them automatically bad, but it does make due diligence non-negotiable.

Primary Residence vs. Investment Property

Buying a home to live in can build equity and provide stability, but that is not always the same as making a strong investment decision. A primary residence may deliver emotional returns, lifestyle benefits, and long-term appreciation, but it also comes with ongoing ownership costs and concentration risk.

Calling every home purchase an “investment” can be technically true and financially misleading. It is better to separate lifestyle decisions from return expectations.

Who Real Estate May Be Best For

- Investors with a long time horizon (typically 7+ years for direct ownership).

- People comfortable with illiquidity and occasional uneven cash flow.

- Those willing to learn underwriting, property management, and compliance basics.

- Investors who value control and tangible assets.

- Households with sufficient cash reserves for repairs, vacancy, and emergencies.

Who May Want to Be Cautious (or Choose Another Route)

- Anyone with minimal cash reserves after the down payment.

- Investors who need quick liquidity or may relocate soon.

- People who strongly dislike operational tasks or conflict management.

- Those already heavily concentrated in one local housing market (job + home + rental in same area).

- Investors chasing appreciation without understanding carrying costs.

A Practical Decision Framework Before You Invest

Run the “Boring Numbers” First

Estimate rent conservatively. Build in vacancy. Budget maintenance and capex. Include taxes, insurance, management, and closing costs. Then stress-test the deal: What happens if rent is 10% lower? What if insurance rises? What if you have one bad turnover year?

Check the Risk You Cannot Renovate Away

You can upgrade flooring. You cannot repaint a flood zone, rewrite local landlord law, or magically lower a bad insurance market. Study these factors early. They often matter more than backsplash choices and “good vibes.”

Compare Against Alternatives Honestly

If a property is projected to produce modest returns with high effort, compare it to alternatives like broad stock index funds, bond funds, or publicly traded REITs. The goal is not to prove real estate is superior. The goal is to choose the option that best fits your return target, risk tolerance, and time capacity.

Extended Experience Section (About ): What Investors Commonly Learn the Hard Way

The most useful lessons about real estate usually come from lived experience, and they are rarely as glamorous as “I bought one house and retired by Tuesday.” Consider a common first-time investor story: someone buys a single-family rental because the monthly payment looks manageable and the area seems popular. On paper, the deal appears solid. In practice, the first year includes a vacancy period, a minor plumbing repair, a higher-than-expected insurance renewal, and a furnace issue that arrives with the emotional timing of a jump scare. The investor does not lose everything, but they do learn the difference between gross rent and actual cash flow. The lesson is powerful: margins matter more than enthusiasm.

Another frequent experience involves investors who do everything “right” operationally but underestimate time. They screen tenants carefully, keep records, respond promptly, and stay compliant. The property performs reasonably well, yet the owner eventually realizes the investment behaves like a small business. There are messages to answer, vendors to coordinate, and decisions to make. Some people love this and go on to build a portfolio. Others decide they would prefer a more passive route, such as REITs, because their career and family already consume their bandwidth. That is not failure. It is good portfolio design through self-awareness.

There is also the experience of buying in a strong market and assuming appreciation will solve everything. Sometimes it does not. Investors who purchase with thin cash flow and high leverage may discover that even a decent property becomes stressful when rates, taxes, or insurance costs rise faster than rent. These investors often become much more disciplined on their next deal: better reserves, stronger underwriting, and a lower purchase price relative to income. Real estate can forgive many mistakes, but it rarely forgives overpaying forever.

On the positive side, patient investors often report that the benefits compound quietly. A property that felt unimpressive in year one can look much better several years later if the loan balance declines, rents improve, and operations stabilize. The investor who kept reserves, maintained the property, and treated tenants professionally may end up with both stronger income and a better asset. In many cases, the real advantage was not market timing but consistency.

One more common experience deserves attention: investors who treat due diligence like a formality tend to pay tuition later. Those who verify lease comps, inspect thoroughly, review insurance options, and understand local rules before closing often avoid expensive surprises. The pattern is consistent across beginner and experienced investors alike. Real estate rewards preparation more than prediction. If there is a universal lesson in the point/counterpoint debate, it is this: real estate can be an excellent investment option, but it is usually a better investment for the prepared than for the impulsive.

Conclusion: The Real Point/Counterpoint Answer

Real estate as an investment option is neither a guaranteed path to wealth nor an outdated trap. It is a tool. In the right hands, bought at the right price, financed sensibly, and managed with discipline, it can generate income, build equity, and diversify a portfolio. In the wrong hands, it can become a cash-hungry stress machine with legal, operational, and liquidity headaches.

The strongest investors do not ask whether real estate is “good” or “bad.” They ask whether a specific deal fits their goals, risk tolerance, time capacity, and alternatives. If you can answer that honestly, you are already ahead of most people on the internet shouting about passive income next to a rented Lamborghini.

Note: This article is for educational purposes only and is not financial, legal, or tax advice. Consult licensed professionals for guidance specific to your situation.