Table of Contents >> Show >> Hide

- The $1B ARR Milestone: What It Signals (and What It Doesn’t)

- Why “Time-to-$1B ARR” Often Doesn’t Predict Long-Term Value

- The Metrics That Matter More Than Speed

- So When Does Speed Matter? (The “Within Reason” Clause)

- How to Go Fast Without Making $1B ARR a Mess

- Experience Notes: What Founders and Operators Learn Chasing $1B ARR (500+ Words)

- Conclusion: The Stopwatch Isn’t the Business

Every SaaS founder secretly wants two things: a product customers love, and a chart that goes up and to the right so aggressively it needs a seatbelt.

And once the chart starts behaving, the next obsession shows up right on schedule: “How fast can we get to $1B ARR?”

Because nothing says “I’m calm and emotionally stable” like benchmarking your company against a handful of once-in-a-generation rocket ships.

Here’s the counterintuitive truth: within reason, the stopwatch usually matters less than people think.

Not because speed is badspeed is great. But because what creates long-term value at (and after) $1B ARR is mostly driven by things that don’t show up in a single “years-to-$1B” headline.

Market size, retention, margins, expansion paths, capital efficiency, and post-$1B execution tend to decide who becomes a durable compounding machine… and who becomes a very expensive treadmill.

The $1B ARR Milestone: What It Signals (and What It Doesn’t)

$1B ARRAnnual Recurring Revenueis a milestone because it suggests you’ve built a product that can produce roughly a billion dollars a year in recurring revenue at a steady-state run rate.

It’s a proxy for scale, distribution, and (usually) enterprise-grade seriousness. You’re no longer “a startup.” You’re an ecosystem. You’re a line item in someone’s budget process.

You’re a topic on earnings callseven if they’re not yours.

But ARR is also a slightly mischievous metric. It’s not always the same as GAAP revenue, it can be influenced by pricing structure (subscription vs. usage-based),

and it can look healthier than the underlying business if churn, discounting, or customer concentration is quietly doing parkour behind the scenes.

So while $1B ARR tells you you’ve reached scale, it does not automatically tell you:

- Whether your revenue is durable (retention quality, renewal risk, customer concentration)

- Whether growth is profitable (unit economics, burn multiple, payback period)

- Whether margins can expand (gross margin, services drag, infrastructure intensity)

- Whether you can keep growing after the easy TAM is exhausted (product expansion and category strategy)

In other words: $1B ARR is a huge achievement. It’s also not the finish line. It’s more like reaching the part of the video game where the villains stop being random

and start having names, backstories, and extremely unfair special powers.

Why “Time-to-$1B ARR” Often Doesn’t Predict Long-Term Value

There’s a reason founders fixate on speed: early-stage SaaS is full of milestone myths. “Fastest to $1M ARR.” “Fastest to $10M.” “Fastest to $100M.”

Speed is visible. Speed is brag-friendly. Speed fits in a tweet. (So does misinformation, but let’s stay focused.)

The issue is that once you’re talking about $1B ARR, you’re comparing businesses that may share the same destination but took entirely different roads.

Some had perfect macro tailwinds. Some built in a giant market. Some have transaction-based components. Some were early and had to educate the market.

Some built a product-led flywheel; others built a sales-led enterprise engine. By the time you hit $1B ARR, you’re not measuring “who is best.”

You’re often measuring “who had the cleanest combination of market, model, and timing.”

Market Size (TAM) Is the Ultimate Cheat Code

If your total addressable market is enormous, you have more room to grow into a very large valuation even if you didn’t hit $1B ARR at warp speed.

A company operating in a massive category (e-commerce infrastructure, cloud data platforms, verticalized mission-critical systems) can compound for longer.

Meanwhile, a company in a narrower niche may hit $1B ARR quickly but eventually run into a ceiling unless it expands the product surface area.

Business Model Shapes the “Value per Dollar of ARR”

ARR is not a universal unit like “meters” or “calories.” A dollar of ARR in one model can be worth more than a dollar of ARR in another.

Why? Because durability, gross margins, expansion dynamics, and pricing power differ.

Subscription-heavy, high gross margin, high expansion models often receive higher long-term confidence than models where revenue is more variable

or requires continuous high-cost acquisition.

Post-$1B Execution Is Where the Real Winners Separate

Getting to $1B ARR proves you can build and sell. Staying great after $1B ARR proves you can execute at scale.

At that point, the questions shift to:

- Can you maintain healthy growth rates while growing margins?

- Can you expand into adjacencies without losing focus?

- Can you reduce reliance on discounts and “heroic” sales efforts?

- Can you scale leadership, systems, and culture without turning into a meeting factory?

If “time-to-$1B” is the opening act, “post-$1B” is the main event. And the main event is longer, harder, and dramatically more lucrative.

The Metrics That Matter More Than Speed

If speed is not the whole story, what is? Think of these as the metrics that keep paying dividends after the milestone confetti gets vacuumed up.

They’re less glamorous than “fastest to $1B,” but they’re far more predictive of whether $1B ARR becomes $2B, $5B, and beyond.

1) Retention: The Compounding Engine

Growth is great. Retention is what makes growth stick.

When retention is strong, revenue compounds. Expansion becomes easier. Sales efficiency improves. Profitability becomes achievable without turning off growth entirely.

When retention is weak, $1B ARR can become an expensive illusionlike filling a bathtub with the drain open and telling everyone you’re “water-positive.”

Two retention lenses matter most at scale:

- Gross retention (how much revenue you keep before expansion)

- Net revenue retention (NRR) (how much revenue you keep after expansion, downgrades, and churn)

Strong net retention means expansion is doing real work. It also means that once you get a customer, the relationship gets more valuable over time.

That’s the kind of business investorsand your future selfcan sleep at night with.

2) Expansion Becomes the Growth Engine as You Scale

Early-stage SaaS is acquisition-heavy: you’re winning logos, proving the use case, and building distribution.

But later-stage SaaS increasingly leans on expansionmore seats, more modules, higher usage, better packaging, and higher willingness to pay.

At meaningful scale, expansion isn’t a “nice to have.” It’s how you avoid stalling.

The practical takeaway: the closer you get to $1B ARR, the more your growth story should include “existing customers love us enough to buy more,”

not just “we can still win new customers with heroic effort.”

3) Rule of 40: The “Are We Creating Value?” Gut Check

The Rule of 40 is popular because it’s simple: growth rate (%) + profit margin (%) ≈ 40.

There are variations (using free cash flow margin, EBITDA margin, etc.), but the spirit is the same:

you’re balancing growth and profitability to indicate healthy value creation.

It’s not a law of physics. It won’t prevent bad decisions. But it is a helpful forcing function.

If you’re growing fast but losing huge amounts of money, that’s a risk profilenot a life philosophy.

If you’re profitable but barely growing, that’s stabilitynot necessarily a compounding growth engine.

Rule of 40 helps you see where you are on that spectrum.

4) Burn Multiple: The “What Are We Paying for Growth?” Reality Check

If Rule of 40 is the big-picture health check, the burn multiple is the receipt.

It asks a blunt question: how much cash are you burning to generate each incremental dollar of net new ARR?

If the answer is “a lot,” you may still reach $1B ARRbut you might arrive carrying a suitcase full of structural problems.

A low burn multiple often signals real product pull and sales efficiency.

A high burn multiple can signal discounting, churn, over-hiring, inefficient channels, or a go-to-market engine that’s working…

in the same way a car “works” when it’s on fire and still technically moving.

5) CAC Payback and Sales Efficiency: Can the Machine Scale Without Breaking?

CAC payback (how long it takes to recover customer acquisition cost) and sales efficiency metrics (like the magic number) matter more as you scale,

because growth becomes less about “can we sell?” and more about “can we sell profitably at volume?”

The goal is to make growth repeatableless dependent on heroics, more dependent on a system.

Here’s the sneaky part: if you sprint to $1B ARR by over-discounting and over-spending, your payback period can quietly become your business model’s

biggest red flag. You’ll feel fast until you try to turn the corner into profitability and realize the steering wheel is… decorative.

So When Does Speed Matter? (The “Within Reason” Clause)

The “probably not” comes with an important qualifier. Speed can mattersometimes a lotwhen the market dynamics reward land grabs or platform capture.

Here are situations where moving faster can meaningfully change outcomes:

Winner-Take-Most Markets

In markets with strong network effects, ecosystem lock-in, or data advantages, speed can help you become the default.

Once you’re the default, you can recruit partners, attract talent, and set standards more easily.

Platform Shifts and Timing Windows

Some waves don’t last forever. If a platform shift opens a windowcloud migration, security posture changes, AI workflow adoptionmoving fast can help you ride

the wave before competitors catch up and before customer attention shifts elsewhere.

Competitive Crowding

If your category is crowded and switching costs are meaningful, speed can help you lock in key accounts and build brand trust early.

In those settings, being “second but better” is possible, but it’s harderand often more expensive.

Capital and Talent Markets

Fair or not, faster-growing companies often attract capital and talent more easily.

That advantage can compoundmore resources can mean faster product development and stronger go-to-market execution.

Of course, the same dynamic can also tempt teams into growth-at-any-cost decisions that create long-term drag. (Congrats, you just invented a future turnaround plan.)

The point isn’t “speed never matters.” The point is “speed is not the primary driver of long-term value once you’re dealing with elite outcomes.”

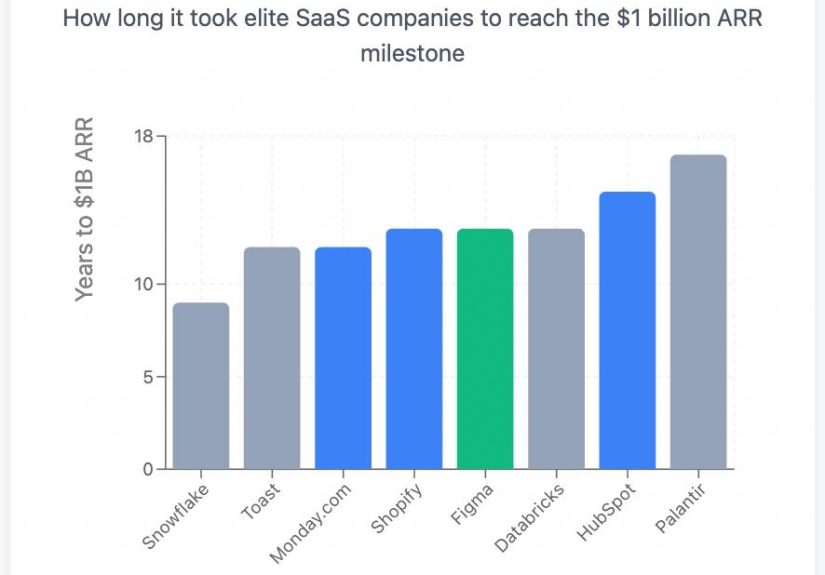

If you get to $1B ARR in 9 years instead of 12, that can be impressive. But if the 9-year path creates fragile retention and messy unit economics,

the “win” can turn into a very expensive lesson in delayed consequences.

How to Go Fast Without Making $1B ARR a Mess

If you want the best of both worldsstrong speed and strong durabilitythink of your strategy as “fast, but clean.”

Here’s a practical way to frame it:

Build a Retention Moat Early

- Track retention by cohort, segment, and use casedon’t average away your problems.

- Invest in onboarding and time-to-value like it’s a revenue lever (because it is).

- Make expansion easy: packaging, add-ons, seat growth, and clear upgrade paths.

Price Like You Intend to Exist for a While

- Discounting can buy ARR today and churn tomorrow. Use it with intention.

- Align price with value deliveredespecially as your product becomes more mission-critical.

- Keep contracts and renewals simple enough that your customers don’t need legal therapy.

Make Growth Efficient Before You Add Fuel

- Monitor CAC payback and burn multiple as “speed limits” for scaling spend.

- Use customer success and product to reduce dependency on paid acquisition.

- Don’t confuse hiring with progress. (Your org chart is not your product.)

Design the Post-$1B Product Roadmap Before You Get There

- Have a believable multi-product strategyor a platform expansion storybefore your core market matures.

- Plan for internationalization, enterprise features, and operational scale early enough to avoid “big company surprises.”

- Keep the customer’s workflow central. The best expansion is the kind customers thank you for.

If you do these things well, the exact year you cross $1B ARR becomes less important than what the business looks like when you arrive:

retention strength, margin profile, and a credible path to keep compounding.

Experience Notes: What Founders and Operators Learn Chasing $1B ARR (500+ Words)

Since we can’t all casually “become a $1B ARR company” between Tuesday and Friday, it helps to learn from patterns founders and operators consistently report

when they get deep into scale. Consider these “experience notes” as a composite of common lessonswhat teams tend to discover once the numbers get big enough

that every small mistake becomes a large mistake with a PR strategy.

1) Speed feels amazing… until it shows up as organizational debt.

Fast growth is a dopamine machine. Pipelines look full. New hires appear weekly. Customers sign. The vibe is immaculate. Then one day, the company realizes

it’s running three different go-to-market motions with five definitions of “qualified,” and nobody can explain why churn rose two points last quarter.

The lesson isn’t “don’t grow fast.” The lesson is “fast growth multiplies system weaknesses.” If your onboarding is shaky at $10M ARR, it’s catastrophic at $100M.

If your product analytics are messy early, you’ll be guessing later when guessing is expensive.

2) The most underrated milestone is not ARRit’s repeatability.

Teams chasing $1B ARR often say the turning point was not a single big deal, but the moment growth became repeatable:

predictable lead channels, a sales motion with consistent win rates, and a customer success model that reliably produced expansions.

Once growth is repeatable, you can scale responsibly. Without repeatability, scaling is basically performance art with payroll.

3) Retention problems don’t announce themselves as “retention problems.”

They show up as discount pressure. As longer sales cycles. As rising support load. As “customers aren’t adopting the advanced features.”

Many teams report that retention improved only after they treated adoption as a product problem, not a customer success problem.

They invested in time-to-value, reduced complexity, fixed confusing workflows, and improved how the product demonstrated value automatically.

The result: expansions felt less like “upselling” and more like “the customer naturally grew into the platform.”

4) The best companies don’t just sell morethey sell smarter.

As ARR scales, founders often discover that “more deals” isn’t the same as “better growth.”

The most durable businesses get picky: they sharpen ICP, they avoid chronically unprofitable segments, and they stop chasing revenue that’s likely to churn.

That restraint can feel slow in the short term, but it often speeds up compounding because the customer base gets healthier and more expandable.

In practice, many teams learn to prefer growth that improves future growthcustomers with high retention, strong usage, and clear expansion paths.

5) Post-$1B ARR success is frequently a product strategy story, not a sales story.

Getting to $1B ARR often requires elite go-to-market execution. Staying great after $1B ARR often requires product expansion, platform depth, and new categories.

Teams report that the “next chapter” is won by building adjacent modules, moving upmarket (or downmarket) thoughtfully, and creating workflows that make the product

harder to replace. When that product strategy is clear, the exact timing of the $1B ARR milestone becomes less emotionally important.

You stop asking, “Are we fast enough?” and start asking, “Are we building something that will compound for a decade?”

The consistent theme across these experience notes is simple: speed is celebrated, but durability is rewarded.

Within reason, $1B ARR is not a race against other companiesit’s a race against entropy. The companies that win are the ones that show up at scale with clean

retention, strong unit economics, and an expansion story that customers genuinely want.

Conclusion: The Stopwatch Isn’t the Business

If you can get to $1B ARR fast, fantasticjust don’t confuse “fast” with “best.” Within reason, long-term value is more strongly influenced by

market size, retention, expansion dynamics, margins, and capital efficiency than by the exact year you crossed an arbitrary threshold.

The goal isn’t to hit $1B ARR as quickly as possible at any cost.

The goal is to hit $1B ARR with a business that’s strong enough to keep compoundingso the next billion is easier, cleaner, and far more profitable.