Table of Contents >> Show >> Hide

- What “The Rorschach Test” Episode Is Really About

- Berkshire Hathaway: The Market’s Ultimate Inkblot

- Charlie Munger at 95: The Compounding of Temperament

- VC Money and the Strange Afterlife of Bad Business Models

- Recession Calls That Won’t Age Well: Forecasting vs. Decision-Making

- Jeopardy!’s New Champ: A Masterclass in Playing the Real Game

- Surveys of the Week: Are Investors Actually Getting Smarter?

- Why Everyone Thinks It Was Better 50 Years Ago

- Putting It All Together: The Episode’s Core Investor Lesson

- Experiences Related to “The Rorschach Test” (500+ Words)

- Conclusion

If you’ve ever stared at a Rorschach inkblot and thought, “That’s definitely a bat,” congratulations: you’ve met your brain’s favorite hobbyturning ambiguity into certainty.

Animal Spirits Ep. 81: “The Rorschach Test” takes that exact idea and drops it into the market, where uncertainty wears a suit, speaks in headlines, and occasionally tweets in all caps.

In this episode, hosts Ben Carlson and Michael Batnick use a clever lens: some companies, trends, and narratives behave like market inkblots.

Investors don’t just analyze themthey project onto them. You don’t merely “have an opinion” about Berkshire Hathaway, venture capital–funded startups, recession calls, or the state of investing today. You reveal your temperament.

And if that sounds too psychological for a finance podcast, don’t worrythis is still markets. There’s plenty of data. We just carry it around like emotional support statistics.

What “The Rorschach Test” Episode Is Really About

Episode 81 moves fast and covers a wide range of ideas, but the connecting thread is this:

the same set of facts can produce wildly different conclusions depending on the storyteller.

That’s not just a media problem. It’s an investor problembecause we are all the storyteller in our own heads.

Key topics discussed in the episode

- Berkshire Hathaway as the market’s Rorschach testwhat investors “see” says as much about them as it does about the stock.

- Charlie Munger still going strong at 95longevity, discipline, and the rare skill of not saying the quiet part quietly.

- Venture capital money and why some companies avoid bankruptcy longer than you’d expect.

- Recession calls that may not age wellforecasting, fear, and the business model of being “cautious.”

- Lessons from Jeopardy!’s new champstrategy, game theory, preparation, and exploiting the rules the way they actually work.

- Surveys of the week and the broader theme that investors are getting smarter (or at least cheaper).

- Nostalgia trapswhy people always think things were better 50 years ago (even when they were wearing objectively worse pants).

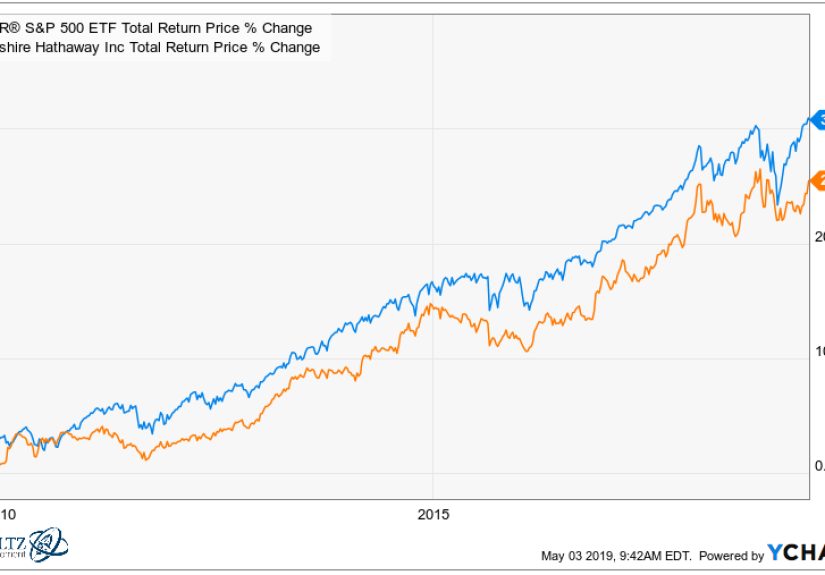

Berkshire Hathaway: The Market’s Ultimate Inkblot

Calling Berkshire Hathaway “the market’s Rorschach test” is a deceptively sharp line. Berkshire is massive, complex, and famously idiosyncratic:

part insurance company, part industrial powerhouse, part Apple proxy, part capital allocation machine, and part living museum of long-term investing.

That makes it usefulbut also incredibly easy to interpret in whatever way supports your existing worldview.

How different investors “see” the same Berkshire

Consider how the exact same conglomerate can produce opposite takes:

- The Value Purist: “A fortress balance sheet, disciplined capital allocation, real cash flow. This is what investing is supposed to be.”

- The Growth Skeptic: “It’s too big. The law of large numbers is undefeated. This is a slow-moving cruise ship.”

- The Macro Worrier: “Look at the cash pileclearly Buffett sees trouble coming.”

- The Macro Optimist: “Look at the operating businessesBerkshire is built for any environment.”

- The Index-Fund Realist: “I can’t ‘understand’ Berkshire, so I’ll just own the whole market. Problem solved.”

The trick is that many of these views can be argued convincingly at the same time. Berkshire can be both a high-quality business and a challenging comp in a market obsessed with

faster stories. That ambiguity is what makes it such a powerful market narrative mirror.

The investing takeaway

When you feel certain about what Berkshire “means,” pause and ask:

Am I analyzing, or am I projecting? The market rewards analysis eventually. Projection gets rewarded only when the crowd happens to share your mood.

That’s less “strategy” and more “weather report.”

Charlie Munger at 95: The Compounding of Temperament

The episode also highlights Charlie Munger still going strong at 95, which isn’t just a fun factit’s a reminder of what long-term thinking looks like in human form.

Munger’s public persona has always been a mix of sharp humor, zero patience for nonsense, and a devotion to mental models.

But the bigger point isn’t “be witty at advanced ages.” It’s this: in markets, your biggest edge often isn’t intelligence.

It’s temperament. The ability to stay calm when the crowd is panicking. The ability to wait when the crowd is itching.

The ability to admit “I don’t know” without immediately replacing it with a confident-sounding guess.

Why temperament compounds

Investors love the idea of compounding returns, but “compounding behavior” matters too:

- Not panic-selling during volatility compounds into more time in the market.

- Sticking to a simple plan compounds into fewer self-inflicted mistakes.

- Avoiding constant prediction compounds into better decision hygiene.

Munger’s longevity in markets is a metaphor: you don’t need to win every day. You need to avoid losing your mind on the important ones.

VC Money and the Strange Afterlife of Bad Business Models

One of the episode’s most modern themes is how venture capital can keep companies alive longer than traditional finance might allow.

In a low-rate world (and even in a “funding is tighter now” world), some startups survive not because the business model works today,

but because the story might work tomorrowand someone is willing to finance the gap.

Why this happens

In classic capitalism, bankruptcy is the reset button. In venture-backed capitalism, you sometimes get a “pause” button:

bridge rounds, down rounds, extensions, restructurings, and strategic pivots that basically translate to, “We’re not dead, we’re… rebranding.”

The episode’s point isn’t that all VC-funded companies are doomed. Plenty become durable winners. The point is that

capital availability changes the timeline of consequences.

And when consequences get delayed, investors can start mistaking survival for success.

A practical investor lens

If you invest in public markets, this still matters because venture cycles influence IPO quality, valuations, and the “story inventory”

that eventually reaches retail portfolios. When money is easy, more stories make it to the public stage. When money is tight,

the market becomes less forgiving, and fundamentals get louder.

Recession Calls That Won’t Age Well: Forecasting vs. Decision-Making

Recession talk is a permanent feature of financial media because it’s useful. Not necessarily useful for investorsbut useful for attention.

“Everything is fine” rarely breaks the internet. “Storm approaching” always does.

Episode 81 nods at a specific kind of prediction problem: recession calls can be correct in theory but wrong in timing,

and the timing is the part that destroys portfolios.

If you go defensive too early, you can miss years of compounding. If you go defensive too late, you get the emotional experience

of learning that “risk” is not just a finance termit’s a feeling in your stomach.

Why people keep making dramatic calls anyway

- It feels responsible: Warning sounds smart. Celebration sounds reckless.

- It’s hard to disprove quickly: “A recession is coming” can be stretched indefinitely.

- Memory is selective: We remember the one time a bear called it right and forget the twelve times they didn’t.

The investing takeaway

Build a plan that works without needing perfect macro timing. If you must have a view, express it with humility and position sizing,

not with an all-or-nothing portfolio personality transplant.

The goal isn’t to predict the next recession. It’s to make sure a recession doesn’t force you into permanent bad decisions.

Jeopardy!’s New Champ: A Masterclass in Playing the Real Game

The episode draws lessons from the then-new Jeopardy! phenomenon who dominated by understanding incentives, probabilities, and the rules.

That story resonated because investing is full of “games” where most people play the version they wish existed, not the one in front of them.

What translates to investing

- Edge is often structural: Strategy can matter as much as knowledge.

- Preparation beats vibes: Systems outperform moods over time.

- Bet sizing matters: Even great answers don’t help if you wager poorly.

In markets, you can be “right” and still lose money if you’re early, overlevered, or emotionally unable to hold through volatility.

Jeopardy! rewards boldness with rules; markets reward boldness only when it’s paired with risk management.

Otherwise it’s not boldnessit’s a jump scare.

Surveys of the Week: Are Investors Actually Getting Smarter?

“Smarter” is a loaded word. But investors have undeniably become more cost-aware and more process-aware over time.

Index funds and ETFs made diversification and low fees more accessible. Online brokers lowered friction. Financial education improved.

And marketsthrough repeated humiliationtaught people that overconfidence is expensive.

What “smarter” can look like in practice

- More people understand that fees matter over decades.

- More investors accept that “doing less” can be a strategy.

- More portfolios focus on long-term allocation instead of short-term predictions.

Of course, new temptations appear every year. The internet can teach you asset allocation and also convince you that a stock chart is “sending signals from the future.”

Progress is real, but so is the human talent for finding new ways to panic with better Wi-Fi.

Why Everyone Thinks It Was Better 50 Years Ago

The episode also touches a classic bias: people tend to remember the past as simpler, kinder, and somehow more competent.

In markets, that becomes “they don’t make investors like they used to” or “back then, fundamentals mattered.”

Here’s the funny thing: every decade thinks the previous decade was more rational.

And every decade produces receipts proving it was not.

Humans are extremely good at building highlight reels. We forget the boring parts, the confusing parts, and the parts where everyone was wrong.

We remember the tidy narratives and the winning trades.

How nostalgia becomes a portfolio problem

- You chase “how it used to work” instead of adapting to how it works now.

- You misread risk because the past feels safe in hindsight.

- You over-trust old patterns and underweight new realities (like market structure changes or fee compression).

The healthiest market mindset isn’t “everything is worse now.” It’s “everything is different nowand different doesn’t come with a moral judgment.”

Markets evolve. Investors evolve. And your job isn’t to romanticize the past. It’s to build a strategy that survives the future.

Putting It All Together: The Episode’s Core Investor Lesson

Animal Spirits Ep. 81 isn’t asking you to become a psychologist. It’s asking you to notice when you’re doing the most human thing possible:

turning uncertainty into a story and then mistaking the story for reality.

Berkshire Hathaway becomes a market inkblot. Venture-backed firms become a morality play. Recession calls become a personality type.

Jeopardy! becomes a case study in incentives. Nostalgia becomes a filter that edits out the messy parts.

And through it all, the market keeps doing what it always does: moving forward with or without your narrative consent.

A simple checklist inspired by the episode

- Separate facts from interpretations. Write them down as two different lists.

- Audit your certainty. If you feel “absolutely sure,” you might be projecting.

- Prefer processes over predictions. A good plan beats a perfect forecast you’ll never make.

- Use humility as risk management. Position sizing is where wisdom becomes real.

- Beware nostalgia. The past is not a strategy; it’s a story.

And if all else fails, remember: the market is an inkblot that charges admission. Try not to pay extra for the deluxe edition of your own biases.

Experiences Related to “The Rorschach Test” (500+ Words)

One of the most relatable parts of Animal Spirits Ep. 81: “The Rorschach Test” is how quickly it maps onto everyday investing experiencesespecially the moments you don’t put in a spreadsheet.

People often think investing mistakes happen because they “didn’t know enough.” But many of the most common missteps happen because they felt something strongly enough to treat it as truth.

That’s the Rorschach effect in real life: ambiguity shows up, and we color it in with our preferences.

A common experience goes like this: an investor sees Berkshire Hathaway mentioned in the newsmaybe around an annual meeting, a big holding, or a quarter where the stock didn’t do much.

If they’re already skeptical about “old school” investing, they interpret the same facts as proof that Berkshire is outdated, too big, and stuck in the past.

If they’re already inclined toward quality and patience, they interpret it as proof that consistency and cash flow still matter.

Nothing changed about Berkshire in that moment. The investor did. Or more precisely: the investor’s lens did.

Another experience shows up during periods of easy money (or even just the memory of easy money).

People hear about venture-backed companies staying alive, raising another round, and “extending runway,” and they subconsciously translate that into,

“See? The market rewards innovation.” Sometimes that’s true. Other times, it’s just survival funded by optimism.

The experience for investors is confusing because it feels like the rules changed: businesses that “should” fail don’t fail on schedule.

And that creates a dangerous habitassuming every surprising survival story is a hidden genius story.

In reality, a lot of it is timing, liquidity, and how long capital is willing to wait for the plot twist.

Then there’s the recession-call experience, which many investors could describe without even looking at their brokerage statement.

It often starts with a headline that feels responsible: “Warning signs flashing.” Someone cuts risk, moves to cash, or stops investing.

At first, it feels like discipline. But as months pass and markets keep moving, the emotional equation changes:

discipline turns into frustration, frustration turns into second-guessing, and second-guessing turns into reactive decisions.

The weird part is that the investor may still be “right” about risks existingrisks always existbut the portfolio outcome can still be worse

because the timing costs more than the original risk would have.

This is where the episode’s theme hits hard: it’s not enough to identify uncertainty. You have to decide how to live with it.

The Jeopardy! segment also matches a real investor experience: learning that “knowing a lot” isn’t the same as “winning.”

Plenty of people can explain the economy, read earnings reports, and define every macro acronym ever invented.

But when it comes time to place a bethow much to allocate, how long to hold, when to rebalancethe winners often look less like geniuses and more like system builders.

They automate contributions. They diversify. They rebalance on purpose. They treat risk like a design constraint, not a dare.

That approach can feel boring, but boring is underrated when your alternative is turning your retirement into a daily drama series.

Finally, nostalgia shows up in a very specific investor experience: remembering the “good old days” of markets that made sense.

People recall an era when “fundamentals mattered,” when “prices weren’t crazy,” when “everyone wasn’t gambling.”

But usually, that memory is curated. The same eras had bubbles, scandals, and plenty of investors doing reckless thingsjust with fewer memes.

The practical lesson many investors learn (sometimes the hard way) is that the goal isn’t to find a perfect market environment.

The goal is to build a portfolio and a mindset that can handle imperfect ones.

That’s why the Rorschach metaphor is so useful: it helps investors recognize that the market isn’t just a place where prices move.

It’s a place where stories formand your job is to make sure your story doesn’t quietly become your strategy.

Conclusion

Animal Spirits Ep. 81: “The Rorschach Test” is a reminder that markets don’t just test your IQthey test your interpretation.

Berkshire, VC-funded survival stories, recession forecasts, and even cultural moments like a Jeopardy! run can become mirrors that reflect what you already believe.

The investing edge comes from noticing when you’re projecting, separating narrative from evidence, and building a plan that doesn’t require perfect predictions to work.

If you take only one thing from this episode, make it this: when the market feels like an inkblot, that’s not your cue to guess harder.

It’s your cue to invest more intentionally.