Table of Contents >> Show >> Hide

- What “Animal Spirits” Means in 2026 (Without the Textbook Headache)

- Scoreboard: The U.S. Economy Right Now

- The Boomflation Case: Why Growth Could Stay Surprisingly Firm

- The Recession Case: Why Downside Risk Still Matters

- Which Scenario Is More Likely in 2026?

- Five High-Signal Indicators to Watch (Monthly)

- Practical Playbook: How to Operate in a Boomflation-vs-Recession World

- Conclusion: Animal Spirits Are AliveBut Not Invincible

- Experience Notes from the Front Lines (Approx. )

If the economy were a movie character right now, it would be the over-caffeinated detective who solves the case,

trips on a rug, and still lands on their feet. That, in one phrase, is today’s “animal spirits” story.

Households are still spending, many businesses are still hiring, and parts of manufacturing are finally waking up.

At the same time, inflation hasn’t fully gone back in its cage, confidence remains jumpy, and forward-looking indicators

keep flashing mixed signals.

This is why the big macro question for 2026 is not just “growth or slowdown?” but a much weirder fork in the road:

boomflation (growth that stays stronger than expected while inflation cools only slowly) versus

recession (where delayed effects of tight policy and fragile sentiment finally bite).

Both stories have real evidence behind them. Both can sound persuasive at dinner parties. Only one can dominate the next 12 months.

In this deep dive, we’ll break down what “animal spirits” actually means in a modern economy, score the current U.S. data landscape,

stress-test both scenarios, and build a practical playbook for businesses, investors, and households. No crystal ball.

No melodrama. Just signal over noisewith a little humor so your coffee doesn’t feel lonely.

What “Animal Spirits” Means in 2026 (Without the Textbook Headache)

“Animal spirits” is economist shorthand for the emotional, behavioral engine behind risk-taking: the confidence that gets

entrepreneurs to expand, consumers to spend, and investors to fund tomorrow before tomorrow arrives. It’s not irrational madness.

It’s the human layer of economicsthe part no spreadsheet fully captures.

In practical terms, animal spirits are visible in:

- Consumers buying discretionary items even when headlines sound scary.

- Small businesses planning inventory and hiring instead of freezing in place.

- Executives approving capex and AI spending despite policy uncertainty.

- Credit markets staying open and financial conditions not tightening sharply.

The catch: animal spirits can pivot fast. They amplify good news and bad news alike. That’s why the current cycle feels strange:

hard data still points to expansion in many areas, while sentiment and leading indicators remain cautious.

It’s like driving with one foot on the gas and one foot hovering over the brake.

Scoreboard: The U.S. Economy Right Now

1) Growth: Still Positive, Not Explosive

Real GDP growth in the latest official quarterly update came in strong, and nowcasts suggest continued expansion into late 2025/early 2026.

That does not scream “recession already here.” It does suggest the economy has more momentum than many expected after rate hikes.

However, momentum can fade quickly if hiring cools and real incomes flatten.

2) Inflation: Better Than Peak Panic, Still Not a Victory Lap

Inflation has moderated substantially from its worst phase, but the path to a stable, low-inflation environment remains uneven.

Core measures are cooler than before, but shelter and service categories keep the descent gradual, not dramatic.

Translation: inflation is less of a fire alarm, more of a smoke detector that still chirps at 2:17 a.m.

3) Labor Market: Slower, Not Broken

Payroll growth has decelerated and unemployment is higher than the ultra-tight lows, yet the labor market still looks more like

“normalization” than collapse. That distinction matters. Recessions usually involve a sharper labor break, not just a cooler job machine.

4) Sentiment and Leading Signals: Mixed Bag, Extra Complicated

Consumer sentiment remains soft relative to pre-pandemic norms. Small-business optimism has improved, but uncertainty is still elevated.

Some leading indexes continue to decline, while purchasing-manager data shows pockets of reaccelerationespecially as manufacturing

exits a long contraction streak and services remain in expansion.

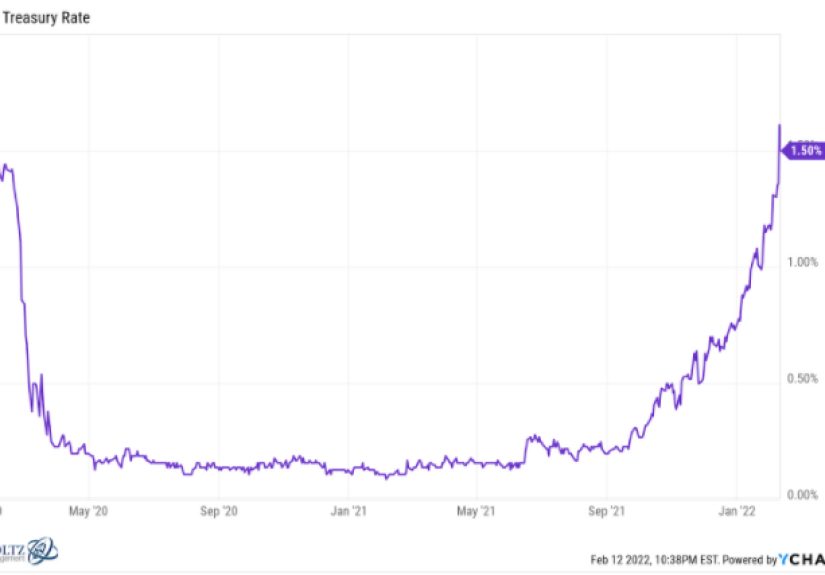

5) Financial Conditions: Looser Than Recession-Scare Narratives Suggest

Broad financial conditions are not especially tight by historical standards, and that helps explain why growth has held up.

If credit stays available and risk premia remain contained, the expansion can persist longer than consensus expects.

If conditions tighten abruptly, the outlook can shift fast.

The Boomflation Case: Why Growth Could Stay Surprisingly Firm

Consumer Muscle Hasn’t Fully Faded

Consumer spending keeps finding ways to surprise on the upside, especially in services and digital retail channels.

Even with higher rates, wage income and employment levels have prevented a broad spending collapse.

If real incomes keep inching up and gasoline stays manageable, households can continue supporting GDP.

Business Sentiment Is Cautiousbut Not Frozen

Small firms report better conditions than during the worst inflation shock, and many executives still prioritize productivity investments.

AI-related capex, process automation, and supply chain redesign are not “hype-only” themesthey are margin and resilience projects.

That’s classic animal spirits behavior: uncertain backdrop, but selective risk-taking where payoffs look tangible.

Manufacturing Is Showing Signs of Life

After a long contraction period, manufacturing gauges have moved back into expansion territory.

No, this doesn’t guarantee an industrial boom. But it does matter for the narrative: the economy is not rolling over uniformly.

A broadening recovery in orders and production would support the boomflation thesis.

The Fed Isn’t Trying to “Crash” the Economy

Current policy communication suggests a data-dependent stance rather than panic tightening.

If inflation drifts lower without a labor-market break, the policy path can remain stable enough to preserve growth.

In that world, boomflation is basically “decent growth + sticky-ish disinflation,” not “1970s rerun.”

The Recession Case: Why Downside Risk Still Matters

Lag Effects Are Real (and Usually Rude)

Monetary tightening works with long and variable lags. Corporate refinancing cliffs, tighter lending standards, and slower hiring

can all arrive after the headline panic has faded. Recessions often start when everyone says, “Huh, that was milder than expected.”

Confidence Is Fragile

Consumers can keep spending until a trigger appears: a labor wobble, market correction, policy shock, or energy spike.

Confidence data still indicates caution, and leading indexes remain soft. Animal spirits can power growth, but they can reverse quickly.

Policy and Geopolitics Can Reprice Risk Overnight

Trade disruptions, fiscal fights, or geopolitical stress can hit prices and demand at the same time.

That’s the ugly version of “boomflation”: costs rise, confidence falls, and growth slows.

If that mix persists, recession odds climb even without a dramatic initial trigger.

Household Balance-Sheet Stress Is Uneven

Aggregate data can hide stress pockets. Lower-income households and heavily indebted borrowers are more rate-sensitive.

Delinquencies in certain categories and tighter consumer credit conditions can become leading stress signals before unemployment jumps.

Which Scenario Is More Likely in 2026?

Right now, the evidence leans toward a slower-expansion baseline, not an immediate recession and not a runaway boom.

Think of it as “good-enough growth with stubborn pockets of inflation risk.”

That puts the economy in a narrow corridor:

- If hiring stays stable and inflation gradually cools, boomflation-lite (resilient growth + sticky disinflation) is likely.

- If labor softens sharply, confidence cracks, or credit tightens, recession probability rises quickly.

In other words, the next chapter depends less on one big headline and more on a sequence of “small but persistent” data moves.

Watch trend direction, not single prints.

Five High-Signal Indicators to Watch (Monthly)

1) Unemployment and Payroll Breadth

One weak payroll month can be noise. Several weak months plus rising unemployment is a different story.

Watch not just total jobs, but whether weakness broadens across sectors.

2) Core Inflation Momentum

Year-over-year inflation gets headlines, but monthly core momentum tells you if disinflation is truly progressing.

Sticky services inflation is the key swing factor for policy.

3) Consumer Spending Mix

If spending shifts heavily into essentials while discretionary categories fade, animal spirits are weakening.

A balanced mix usually supports the soft-landing/boomflation-lite path.

4) PMIs and Small-Business Plans

PMIs above 50 and improving small-business expectations suggest real-economy confidence is holding.

A synchronized dip below expansion thresholds would be an early warning.

5) Financial Conditions and Yield Curve Behavior

If financial conditions stay loose and curve signals normalize without stress, growth can persist.

If spreads widen and credit tightens abruptly, recession risk can accelerate faster than most forecasts assume.

Practical Playbook: How to Operate in a Boomflation-vs-Recession World

For Business Owners

- Run two budgets: base case (slow expansion) and downside case (demand dip).

- Prioritize productivity capex over vanity capex.

- Lock in financing where possible before credit conditions shift.

- Protect margin with pricing discipline, not panic discounting.

For Investors

- Favor balance-sheet quality and cash-flow durability over story stocks alone.

- Use barbell exposure: resilient defensives + selective cyclical upside.

- Keep dry powder; volatility is a feature, not a bug, in mixed cycles.

- Track policy expectations, but anchor on earnings and macro breadth.

For Households

- Keep emergency savings liquid (boring is beautiful).

- Refinance or reduce expensive variable-rate debt where possible.

- Budget with an inflation cushion, especially for services.

- Don’t make big decisions on one scary headline.

Conclusion: Animal Spirits Are AliveBut Not Invincible

So, boomflation or recession? The honest answer today is: the U.S. economy is still running on animal spirits, but with a thinner margin for error.

Growth is real. Inflation progress is real. Policy risk is real. Confidence fragility is real.

If the labor market bends without breaking and inflation keeps easing, the likely outcome is continued expansion with occasional “are we there yet?” moments.

If confidence and credit crack together, recession odds rise fast. Until one side clearly wins, this is a cycle that rewards flexibility, data discipline,

and fewer dramatic predictions from people who also predicted nine of the last two recessions.

Experience Notes from the Front Lines (Approx. )

The most useful way to understand “animal spirits” is to look at lived, day-to-day decisions. Not abstract chartsactual behavior.

Consider three composite experiences based on common patterns seen across U.S. households and businesses this year.

Experience 1: The Main Street Owner Who Refused to “Wait for Perfect”

A mid-sized neighborhood restaurant group had every excuse to freeze spending: rent pressure, wage pressure, and wildly inconsistent

demand on weekdays. Instead, the owner made a very unsexy investment: kitchen workflow software, better prep scheduling,

and a tighter menu engineered for ingredient overlap. No flashy expansion. Just operational intelligence.

Six months later, labor hours per cover fell, food waste dropped, and table turn times improved enough to lift revenue in peak windows.

Did inflation vanish? No. Did uncertainty disappear? Also no. But this was pure animal spiritsconfidence expressed through disciplined risk-taking.

The owner didn’t “bet on boom times.” She bet on productivity while uncertainty remained high. That’s a boomflation survival move:

protect margin first, then grow.

Experience 2: The Household That Stopped Doomscrolling and Started Scenario Planning

A dual-income family with two school-age kids felt stuck in permanent macro anxiety. Every month had a new headline:

recession warning, inflation scare, market rally, policy dramarepeat. Their breakthrough wasn’t finding a better prediction.

It was building a better system: three spending tiers (essential, flexible, optional), automatic transfers to emergency savings,

and a debt paydown sequence targeting the highest variable-rate balance first.

Over nine months, they reduced interest expense, stabilized cash flow, and created room for occasional discretionary spending without guilt.

Their personal economy became anti-fragile. Ironically, once they felt less fragile, they spent more rationally, not more fearfully.

That’s what animal spirits look like at household level: confidence from structure, not from vibes.

Experience 3: The Manufacturer That Saw a Turning Point Before the Headlines Did

A regional components manufacturer spent most of the prior year in defensive mode, assuming orders would remain soft.

Then two things shifted: inquiries rose from existing clients, and lead-time conversations stopped sounding panicked.

Management didn’t go full throttle. They added one targeted hiring cohort, restarted a paused training program,

and negotiated supplier terms with volume flexibility instead of rigid commitments.

The result: when orders improved, they captured upside without overcommitting fixed costs.

Their leadership team called it “optimistic caution”a phrase that perfectly captures this cycle.

They weren’t predicting a boom; they were preparing for optionality.

Across all three experiences, the pattern is clear. People and firms aren’t waiting for macro certainty, because it never arrives in gift wrap.

They’re choosing practical bets with asymmetric payoff: downside contained, upside available.

That is the real-world signature of animal spirits in 2026.

If recession comes, these behaviors still help absorb the shock.

If boomflation persists, these behaviors compound gains.

Either way, the winners are not the loudest forecasters. They are the best adapters.