Table of Contents >> Show >> Hide

- What Does “MICR Account Number” Mean?

- The MICR Line, Explained Like You’re a Normal Human

- Where to Find Your MICR Account Number

- What People Use MICR Account Numbers For

- MICR Account Number vs. Routing Number vs. Check Number

- How to “Read” the MICR Line Without Guessing

- Common Problems (And How to Avoid Them)

- Is It Safe to Share Your MICR Account Number?

- FAQ: Quick Answers About MICR Account Numbers

- Real-Life MICR Moments: 500+ Words of “Yep, Been There” Experiences

- Conclusion

Those weird-looking numbers at the bottom of a paper check? The ones that look like they were printed by a very confident robot from 1987? That’s the MICR line, and inside it lives the thing people often call a MICR account number.

Here’s the twist: there usually isn’t a separate “MICR account number” hiding in your bank like a secret level in a video game. In most cases, it’s simply your bank account number as it appears in the MICR line (printed in magnetic ink, in a special font, in a special spot). That formatting is what makes it “MICR.”

In this guide, you’ll learn what the MICR account number means, where to find it (with and without checks), how it differs from your routing and check numbers, and how to handle it safelybecause yes, it’s useful, and yes, you should treat it like the financial equivalent of leaving your house key under the “obvious fake rock.”

What Does “MICR Account Number” Mean?

MICR stands for Magnetic Ink Character Recognition. Banks use MICR technology to read and process checks quickly and accurately. The MICR line is printed using magnetic ink (or toner) and a standardized, machine-friendly font. That’s why the numbers don’t just look differentthey’re designed to be read by high-speed sorting and scanning equipment.

So when people say “MICR account number,” they usually mean:

- Your account number (the one that identifies your specific checking account) as printed in the MICR line at the bottom of a check.

- Not your debit card number, not your online banking username, not your “member ID,” and definitely not the number on your coffee punch card (tragically).

Bottom line: the “MICR” part refers to how the number is printed and read, not a different kind of account.

The MICR Line, Explained Like You’re a Normal Human

On most U.S. personal checks, the MICR line contains three main sets of numbers:

- Routing number (identifies your bank)

- Account number (identifies your specific account)

- Check number (identifies that specific check)

Many banks print them in that order from left to right. However, layouts can varyespecially on business checksso it’s smart to confirm using your bank’s labeling (online or in-app) if you’re unsure.

Why the MICR Line Looks “Different”

U.S. checks are typically printed in a MICR font called E-13B, which includes digits and a few special symbols used as separators. Those symbols help banking machines know where one field ends and another begins. You might not see them clearly at a glance, but the equipment does.

Think of the MICR line like a packing label: bank destination (routing) + account “apartment number” (account) + package ID (check number).

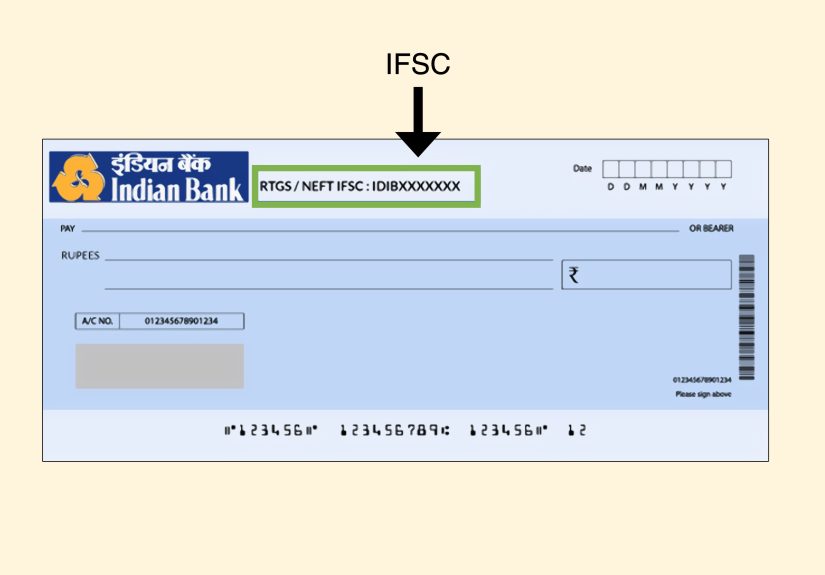

Where to Find Your MICR Account Number

If you have a paper check, finding your MICR account number is simple. If you don’t, you still have optionsbecause modern life is mostly “please don’t mail me anything, ever.”

1) On a Paper Check (The Classic Way)

Look at the bottom of the check. You’ll see a line of numbers printed in a special typeface. On many checks:

- Routing number = first group (usually 9 digits) on the left

- Account number = next group in the middle

- Check number = last group (often on the right)

The MICR account number is typically that middle groupthe account number portion of the MICR line. (And yes, you may also see the check number printed at the top right of the check. That’s normal.)

2) In Your Online Banking or Mobile App

Most major banks let you view your routing and account numbers inside your account details. This is often the best option if you don’t have checks (or if your checks are stored “somewhere safe” that you haven’t found since 2019).

Pro tip: banks sometimes label this as “Account & routing number” or “Direct deposit info”. If you see a toggle for ACH vs. wire routing numbers, pick the one that matches what you’re setting up (more on that later).

3) On a Bank Statement (Sometimes Partial)

Some statements show your full account number; others mask it (e.g., “****1234”). If you need the full number and the statement only shows part of it, go with online banking or call your bank.

4) On a Deposit Slip (Not Always)

A deposit slip may include your account number, but not always the same way it appears in the MICR line. If a form specifically asks for “MICR,” a paper check is the closest match. For most everyday needs (direct deposit, bill pay), the standard account number is what matters.

5) From Your Bank (Direct Deposit Form or Teller Printout)

If you don’t have checks and don’t want to hunt through menus, your bank can provide a direct deposit form or an official printout of your account details. This is common for employers, benefit programs, and payment platforms.

What People Use MICR Account Numbers For

You usually share your routing and account numbers (the same ones found in the MICR line) when you’re setting up electronic payments or receiving money. Common scenarios:

Direct Deposit

Employers, payroll providers, and government agencies use routing + account numbers to send money to your account. Many systems still ask for a “voided check” because it reduces typos and speeds verification.

Automatic Bill Pay and ACH Transfers

ACH transfers (bank-to-bank payments) typically use the routing and account numbersoften collected from a check, a bank form, or an online verification process.

Check Processing and Substitute Checks

Even when checks are processed electronically behind the scenes, the MICR line remains a key identifier. Modern check-handling systems can create a legally recognized “substitute check” image when needed. Translation: that bottom line still matters, even in a digital world.

MICR Account Number vs. Routing Number vs. Check Number

These get mixed up constantly, so here’s the clean separation:

Routing Number

A routing number (also called an ABA routing transit number) identifies the financial institution. It’s typically 9 digits on U.S. checks and helps route the transaction to the right bank.

Account Number

Your account number identifies your specific account at that bank. Length varies by bank. When it appears in the MICR line, people sometimes call it the MICR account number.

Check Number

The check number identifies a specific check in your checkbook sequence. It helps you (and the bank) track checks and spot weird activity. It’s often printed in the top right corner and in the MICR line.

MICR Number / MICR Line

The MICR line is the whole encoded line at the bottom, printed in magnetic ink/toner using a MICR font. It typically includes routing, account, and check numbers (and in some workflows, additional encoded data may appear for processing).

How to “Read” the MICR Line Without Guessing

You don’t need to become a check-forensics expert, but you do want to avoid the most common mistake: mixing up ACH routing numbers with wire routing numbers, or mistaking the check number for the account number.

A Simple Verification Checklist

- Routing number: usually 9 digits, and many banks explicitly label it as routing/ABA.

- Account number: usually the longest “middle” group on a personal check.

- Check number: often shorter, matches the printed number at the top right.

If anything looks inconsistentlike the “account number” being only 3 digitspause and confirm in your bank app. Your future self will thank you.

Common Problems (And How to Avoid Them)

Problem: “My form asks for MICR, but I don’t have checks.”

Ask whether they truly need MICR formatting or simply your routing + account numbers. Many forms say “MICR” when they really mean “banking details.” If they truly need a voided check, ask your bank for a direct deposit letter or official account verification.

Problem: “My check layout looks different.”

Some checks (especially business checks) place the check number in a different spot in the MICR line. Use your bank’s labeled examples or the account details page online.

Problem: “Leading zeros are confusing.”

Don’t drop them. If your account number starts with zeros, those zeros are part of the number. Copy it exactly as shown in your bank’s account details.

Problem: “Someone asked me to text a photo of my check.”

A voided check is commonly requested for legitimate reasons, but “send me a photo of your check over text” is not a universal best practice. If you’re not sure who’s asking, use a safer method: provide routing + account numbers through a secure portal, or use your bank’s direct deposit verification document.

Is It Safe to Share Your MICR Account Number?

Your routing and account numbers are printed on every check you hand outso they’re not secret in the way a card PIN is secret. But they’re still sensitive. In the wrong hands, they may be used to attempt unauthorized ACH debits or to create counterfeit checks.

Smart Ways to Share It

- Use official portals (employer HR system, government site, bank verification tool).

- Verify the request by calling the organization using a trusted phone number.

- Limit photos of checks unless you’re using a secure upload method.

- Monitor your account after sharing details for a new setup.

If you suspect your account details have been misused, contact your bank immediately and review recent transactions. Acting fast matters.

FAQ: Quick Answers About MICR Account Numbers

Is a MICR account number the same as my bank account number?

Usually, yes. It’s your account number as printed in the MICR line on a check. The digits should match your account number in online banking (though formatting and separators differ).

Is the MICR number the routing number?

No. The routing number is one part of the MICR line. The MICR line typically includes routing, account, and check numbers.

Can I find my MICR info on my debit card?

Not reliably. Debit cards use different numbering systems. Use your bank app, statements, or a check.

Do savings accounts have MICR account numbers?

MICR is most closely tied to checks, which are typically drawn from checking accounts. You can still have routing and account numbers for savings accounts for transfers, but they may not be presented as a “MICR line” unless checks are issued for that account type (which is uncommon today).

What if the MICR line is smudged or damaged?

If the check is damaged, ask the issuer for a replacement. For your own account details, rely on your bank’s official account information in online banking rather than trying to “decode” a messy check.

Real-Life MICR Moments: 500+ Words of “Yep, Been There” Experiences

Let’s talk about how MICR account numbers show up in the real worldbecause most people don’t wake up craving check trivia. They stumble into it at the exact moment they’re trying to get paid, pay a bill, or prove they’re a real person with a real bank account.

Experience #1: The New Job Paperwork Panic

You’ve accepted a new job. You’re feeling unstoppable. Then HR sends a direct deposit form that calmly asks for your “routing number” and “account number,” and you suddenly forget every number you’ve ever knownincluding your own phone number. This is where people often grab a check (if they have one) because the bottom line neatly displays the numbers in one place. If you don’t have checks, the bank app becomes your best friend. The “aha” moment is realizing the form doesn’t need anything magicalit just needs accurate numbers, entered exactly, without dropping leading zeros or swapping fields.

Experience #2: The “Voided Check” Treasure Hunt

Some payroll systems and payment platforms still request a voided check. In theory, it’s simple: write “VOID” across a check and hand it over. In practice, it turns into a scavenger hunt through desk drawers, junk mail piles, and that one mysterious folder labeled “IMPORTANT” that contains exactly zero important things. A lot of people learn (the hard way) that it’s smart to keep a single blank check tucked away for admin stuff like thisbecause the day you need it is never the day you can find it.

Experience #3: The Autopay Mix-Up

Setting up autopay feels easy until the confirmation email says “We couldn’t verify your account.” The most common culprit? Someone entered the check number instead of the account number, or accidentally used the wire routing number for an ACH setup (or vice versa). The numbers on a check are close together, and the brain loves to “help” by guessing. The fix is usually boring but effective: open the bank’s account details page, copy the routing and account numbers from the labeled fields, and re-enter them. Suddenly, everything works, and you’re left wondering why your keyboard didn’t come with a “prevent me from being overconfident” setting.

Experience #4: The “Is It Safe?” Debate

People often have a moment of hesitation when asked to share routing and account numbersbecause it feels like handing over the keys to the vault. At the same time, checks literally print those numbers on the front, and humans have been handing checks to other humans for decades. The practical middle ground is learning who you’re sharing with and how. Sharing details through a verified employer portal? Normal. Handing a photo of a check to a random “buyer” online who insists it’s for “verification”? Hard pass. The experience many people come away with is that the numbers themselves are standard, but the context is everything.

Experience #5: The Business Owner’s “DIY Checks” Temptation

Small business owners sometimes discover MICR when they start printing checks for payroll or vendors. The tempting thought is, “It’s just ink and paperhow hard can it be?” Then they learn the MICR line has specific standards, uses magnetic ink/toner, and needs to be printed in a reserved area (the clear band) so machines can read it consistently. The real-life lesson here is that cutting corners on check printing can lead to rejected checks, delays, and headachesso many businesses either order checks from approved printers or use bank-recommended systems rather than winging it with a home printer and pure optimism.

The common thread in all these experiences is simple: MICR account numbers aren’t complicated because they’re mysterious. They’re complicated because they show up when you’re busy, distracted, and just trying to get something done. Knowing where to find themand how to double-check themturns an annoying errand into a two-minute task.

Conclusion

A MICR account number is typically just your regular account number as it appears in the MICR line at the bottom of a checkprinted in magnetic ink so banks can process transactions quickly and accurately. You can find it on a paper check, in your bank’s online account details, or via an official bank form if you don’t use checks.

The best move is also the least exciting: copy the numbers exactly, confirm whether you need ACH or wire details, and share them only through trusted, secure channels. Boring? Yes. Effective? Also yes. And effective is the whole point of money.